Free 34-day trial of YNAB

I'm frugal by nature.

So when there are free alternatives (Excel file or a budgeting app), I'm the first to prefer these over paying for a product.

Except for YNAB.

I tried it for a month, and I've never looked back. It's one of the keys that has helped me achieve my first million Swiss francs - onto the next million(s)!

N.B. you can benefit from a whole year free if you're a university student (anywhere in the world).

YNAB review: Our experience with the best budget app

“What if we never become property owners in Switzerland…?”

It was a rainy Sunday in 2013.

I was at home (in Romandy) with Mrs MP. The little ones were having a nap.

We were once again talking about wanting to be homeowners in Switzerland.

We needed to have CHF 160'000 as a deposit for the house of our dreams.

But instead of dreaming, this time, I decided to calculate all the money that we had put aside.

It took me a while to find all this financial information… on our online banking, in our files, in order to understand the cash value of our respective 3a pillars, etc.

By scraping together every last cent, we ended up with… CHF 48'500

This was a cold hard shock!

That’s when I said to myself:

What if we never become property owners in Switzerland?

This was the defining moment that made us set a budget.

Being the family geek, I spent several evenings the following week looking for the best budget app.

With Excel budget templates and budget apps of dubious quality, it wasn’t easy to make sense of it all.

Until I came across YNAB.

It was a paid budget app but our goal was worth it. Especially as we could trial it for just over a month for free.

The rest is history: I discovered the FIRE movement thanks to the YNAB forum, we bought our home 1 year in advance of our forecast, and we became millionaires (in CHF) less than 10 years after having set up You Need A Budget.

Am I biased in my review? Yes, obviously, otherwise it would be just a list of functionalities that would bore you to death!

Would I go back? Not for anything!

Let’s move onto the YNAB review - a little piece of budgeting software in a bit more of an objective manner.

YNAB review – in a nutshell

In summary, here is my opinion on the YNAB budgeting app, starting with the advantages of YNAB:

What I like about YNAB

- The YNAB method for managing your money, which supports and guides you, rather than just a simple budgeting app. They have four main guiding principles, which changed my life (along with many others). On average, their users save CHF 600 during the first 2 months of use, and CHF 6'000 during the first year. I’m proof of this (we saved even more!)

- Certainty of the accuracy of your budget compared to worrying about making an error in your calculations when you do your budget manually in an Excel file.

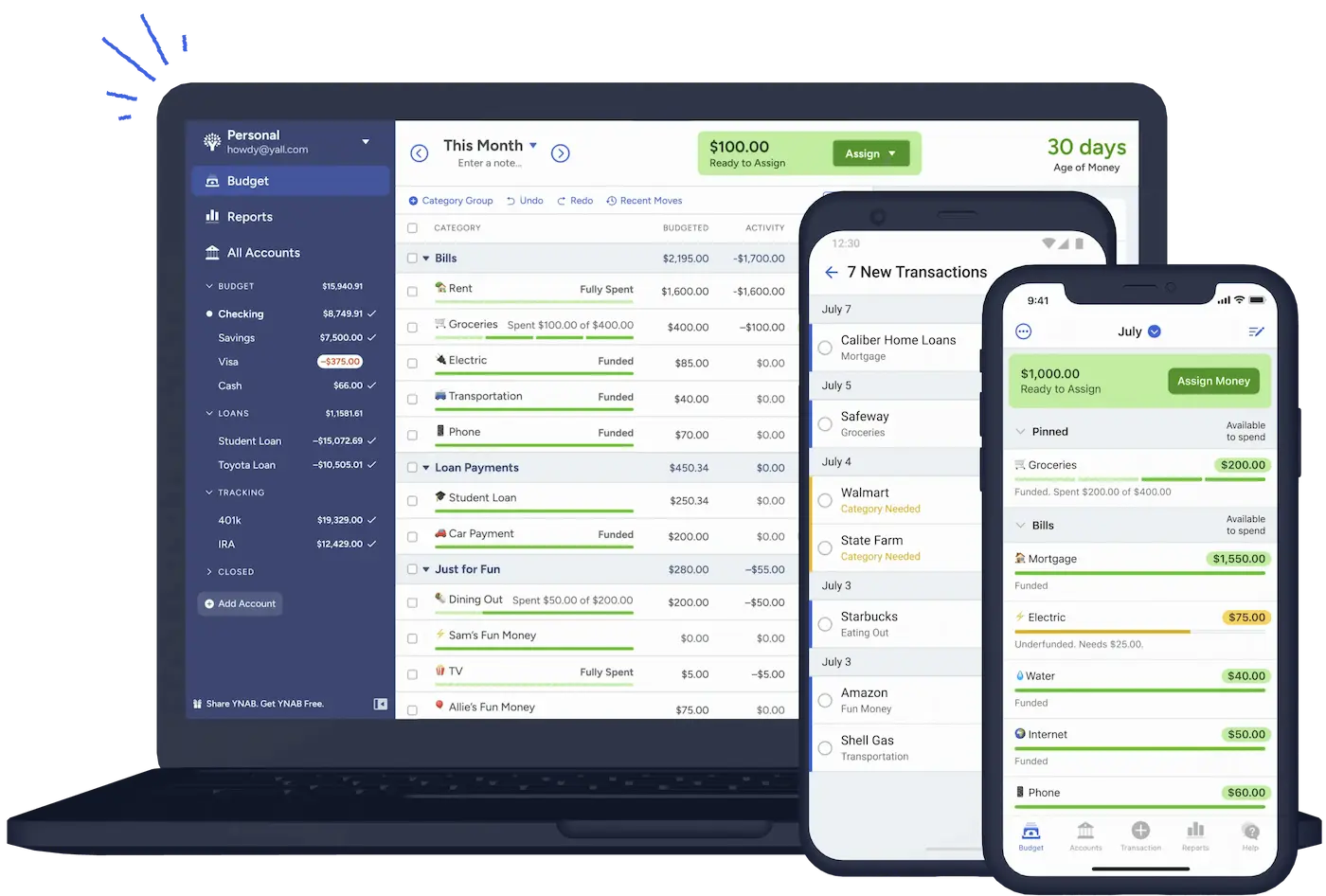

- You Need A Budget is available everywhere, as long as you have an internet connection — and especially on your cellphone. Currently, they have no less than a web app, an iPhone and Android app, an iPad app, an Apple Watch app, and an Alexa app!

- The principle of separate “Budget” and “Accounts” views, which aggregate all your money into one place, and enable you to budget without worrying whether you have 1 or 20 bank accounts.

What could YNAB improve in the future?

- Translate their budgeting app and website into several languages so that the whole world can benefit from it. I’ve been nagging Jesse (the founder of YNAB) about this for years ;) But strategically, they still have so much to do in the USA that it’s not on their roadmap to conquer the rest of the world (especially as AI will surely translate the whole web soon anyway). Nevertheless, I’d recommend you read the green box below about this point.

- Multi-currency management for us Swiss who live in the middle of Europe and often have accounts in CHF, but also EUR and USD. Though I admit we’re a special case. Also, you can manage very well having money flows in other currencies in YNAB, that you convert into your base currency (CHF for us) each time.

- The price of the YNAB app rose in 2024 to 109 USD per year (9.08 USD per month). It’s not trivial but as explained in the introduction, I see it as an investment. I hope that the You Need A Budget team will continue to be frugal with their expenses and investments, and that they’ll stay under the 110 USD per year barrier for even longer.

MP recommendation

For all these reasons, I’m always recommending YNAB to the people around me.

Yes, it’s not cheap, but it’s an investment in the health of my budget, and in the growth of my wealth.

What actually is YNAB?

YNAB is a budget app that provides you with a clear and precise plan for managing your spending and, above all, for saving.

Rather than a budgeting app, I would describe You Need A Budget as a wealth-building tool. And one that you always have to hand.

Effectively, whether you’re sitting at your computer or on a bus, you can access all their platforms which are always synchronized automatically.

YNAB helps you build up your wealth in Swiss francs thanks to its proven method that has been used since 2003.

The YNAB method has 4 rules:

- Rule 1: Give each of your Swiss francs a job

No more looking at your bank account balance to decide whether or not you’re going to buy yourself something. As soon as you receive money, you assign it to something in advance. Then, you just need to follow your plan. - Rule 2: Embrace your true expenses

Anticipate your large non-monthly expenses (hello Christmas presents or your car insurance!) by dividing them up into monthly savings amounts that you put aside to make them smaller and easier to manage. - Rule 3: Roll with the punches

Plans change. So if it turns out that you’re spending more in one expense category, you just need to make an adjustment via a system of communicating pots. No need to feel guilty anymore! - Rule 4: Age your money (aka Live on last month’s income)

It seems so natural to me now but I remember back then that we used to impatiently await our salaries in order to pay the bills that we had waiting. Today, with the YNAB payee management, we always have the cash waiting, even before receiving the bills. And, no joke, it’s become a real pleasure to pay the bills because we have a feeling of control over our financial life!

The YNAB app enables you to centralize all your accounts (bank, brokerage, etc.) in order to have a consolidated overview of your assets.

Alongside that, you have a “Budget” view, which enables you to allocate each one of your hard-earned CHF to a specific goal.

As I often say: if you cut my access to YNAB today, I’d be blind when it comes to our family’s money and assets.

Basically, I no longer even look at my accounts in order to make a spending decision; YNAB consolidates everything, and I use its “Budget” view to make each of our financial decisions.

So for you who are on the path towards financial independence, YNAB is there for the whole area of “Managing your incoming and outgoing money”, and therefore implicitly also for the “Saving” section (so important to make it increase in order to become FIRE one day).

Generally, the question that comes next is: what’s so special about YNAB compared to other budgeting apps?

YNAB review - why it is THE best budget app

YNAB (You Need A Budget) is THE best budget app for monitoring your spending and increasing your savings month after month. This is due to its simple — but extremely effective — method integrated in the software, the YNAB payee managementand and its various apps being available everywhere (web, mobile, tablet, watch).

The Mustachian criteria for choosing the best budget app in Switzerland

Compared to all my other choices of financial products, I know that the YNAB app is the one that can be divisive within the Mustachian community, due to the subscription cost.

But remember that personal finance is “personal” for a reason ;)

So here’s how I judge whether a budgeting app is the best or not:

Criteria 1 - Ease of use (regardless of where you are)

While I don’t mind so much about the complexity of my brokerage account (which I access once a month or quarter), I do think it’s important to have a budgeting app that makes you want to use it.

Especially when you use it every day, and largely “on the move” on your smartphone.

I therefore want it to be intuitive and mobile under these criteria.

Criteria 2 - A proven method

By proven, I mean a method that “really works”, by increasing my net wealth every month!

Criteria 3 - Full encryption of my data

I have my entire financial life saved in my budget app. And as I prefer a solution that is connected across all my devices, I expect full encryption of my data (both when transmitting it as well as storing it).

Criteria 4 - Automatic import of transactions

This criteria is important only after having done 2-3 years of manually importing every transaction. For me, this formative aspect is necessary in order to have a good sense of awareness of your outgoings.

Once you’ve reached the “Ninja / Senior / Master of Budget” status, then a bit of help with automatically importing your transactions is welcome. Whether it’s in CSV import mode or via a direct connection with your various banks and other financial institutions.

YNAB user ratings

As with all the products and services that I use, I like to check the ratings by their current users.

Because while satisfied customers don’t always comment, I can tell you that unhappy customers are the first to post their negative opinions!

From experience, when a mobile app exceeds a score of 4/5 on app stores (AND the app has more than 20-40 ratings), then that reassures me quite a lot.

And how can I tell you…

The YNAB app is a real hit when it comes to ratings… both with the average and the number of reviews it’s received…

I couldn’t believe my eyes! Especially as I hadn’t taken the time to go back and look at this info since 2013:

Average scores of the YNAB iPhone app on the Apple App Store — 50k ratings on the English version of the App Store!

Their number of ratings is crazy.

And you’ll find a screenshot of YNAB reviews below:

You can make your own mind up via these links to the most recent reviews of the YNAB iOS app and the YNAB Android app, depending on your type of smartphone.

The alternative solutions to YNAB — and how they compare

Honestly, I don’t remember which other budget apps I tried out in 2013…

So I had to go to the MP forum to see which budgeting app was being discussed and used back then.

As usual, I present my budget app comparison to you as if we were chatting over a coffee on a terrace in Lausanne or Lucerne.

You Need A Budget vs. Google online spreadsheet (aka Google Sheets)

Google Sheets is the first way in which I started to do our budget. The two main advantages were: easy to set up and free!

Except that after a few weeks, I became aware of the first really annoying thing: a spreadsheet is really not very practical to edit on a smartphone…

After a few months, I rarely updated our budget.

That’s when I looked for another budgeting solution, and I chose YNAB.

For me, YNAB is better than Google Sheets for two key points: firstly, the YNAB method that is 100% integrated with their apps changed my life, and secondly, YNAB can be used everywhere, including on a cellphone.

Oh yes, and thirdly too, Google Sheets is too subject to human calculation errors…

YNAB vs. Beancount

As I’m such a DIY geek when it comes to my financial optimizations in order to become FIRE, I’m really put off by the idea of having a duplicate input record-keeping system with Beancount. What I find lacking the most compared to YNAB: an interface that makes me want to budget (!), and again, the YNAB method!

Also, for the less geeky among us who don’t want to or don’t know how to install Beancount’s Open Source code, it is also available as a paid version at the same price as YNAB. So it’s even easier for me to choose You Need A Budget.

YNAB vs. MoneyWiz

MoneyWiz is like YNAB on steroids, but not in a good way. There is a plethora of functionalities, but the whole thing lacks structure when it comes to how you can or have to use it. The simplicity of YNAB and its method swing it for me.

YNAB vs. Firefly III

When testing the Firefly III demo, I felt like I was using my father’s Quicken of the 2000s… OK I’m exaggerating a bit. But YNAB is designed to be focused on the user and ergonomic, without 10'000 functionalities all over the place. This makes you want to use your budget. And to repeat, the YNAB method does everything.

YNAB vs. Bluecoins

I had to check that Bluecoins was still available on the app stores before mentioning it here (as the latest publication on their website is from 2022…) But yes, the app is still available.

Nevertheless, for me, this budgeting app seems too experimental compared to YNAB, which was set up two decades ago.

I wouldn’t want to find myself one day with an app that is no longer supported (or, even worse, available), and have to start everything over again elsewhere. And if that were to happen with You Need A Budget, I believe that I would know this in advance in a more professional manner.

If you use a digital solution for your budgeting and it is not listed here, let me know via the comments section at the bottom of the page.

How to try out YNAB for the first time

Here is how your YNAB trial will work during the first 34 days:

1. Create your YNAB account

By using this link to create your free YNAB trial account, you’ll support the blog which will earn a small commission, and it won’t make any difference to you. Thanks in advance!

2. Start to make a plan for your money

- Create all your accounts in YNAB by inputting your current balance (don’t worry about importing all your transactions as it’s the future that we’re focusing on!)

- Define your targets to monitor your progression

![Click on button [1] then on [2] (because in Switzerland for the moment, we can't connect our bank account to YNAB so that transactions appear automatically)](/images/ynab_review/en_ynab_add_account_bis.webp)

Click on button [1] then on [2] (because in Switzerland for the moment, we can't connect our bank account to YNAB so that transactions appear automatically)

You can add as many bank accounts as you have (as well as your brokerage accounts and any mortgages).

Also, you can change your base currency to Swiss francs (CHF) from the settings menu.

3. When you spend or earn money

- Assign your Swiss francs to your future expenses and/or savings objectives

- Import your transactions automatically (or manually) in order to monitor your outgoings

- Stress less by knowing that you now have a plan for your money!

Assuming that we're in the middle of the month, and you want to put CHF 1'000 aside for your rent of CHF 1'800, here's how you do it (point 2 represents the amount you have left to assign afterwards)

You’ll see, you even get lots of mini tutorials along the way as you’re using YNAB.

You’re never lost, as the software guides you through each new step.

4. One week before the end of your YNAB trial

- The You Need A Budget team will send you an email to remind you that your trial is about to end

5. The 34th day

- Your trial ends

- Good news: there’s no need to cancel anything as you will only pay if you subscribe voluntarily — that shows you YNAB’s philosophy!

- If you decide to continue, choose a subscription plan (I recommend the annual plan as it’s cheaper) and get rich over the long term!

I strongly recommend you begin with this YNAB starter guide, which can be translated into German or French (by using Google Translate’s automatic translation):

YNAB is the first building block for your life of wealth!

FAQ about YNAB

Who created You Need A Budget?

YNAB, or You Need A Budget, was created by Jesse Mecham in 2003. Initially, it was for his own use with his wife, Julie. But on seeing how his YNAB method had become indispensable to them, he decided to mention it to others. It then had a snowball effect.

He therefore launched “You Need A Budget” as a product in 2004.

I had the honor of chatting with Jesse for over an hour during an interview especially for the readers of the MP blog:

Where is the YNAB head office?

The “You Need A Budget LLC” head office is in Lehi, Utah, in the USA.

What is the “YNAB method”?

The YNAB method is a set of 4 rules established by Jesse Mecham. By following these rules alongside using the YNAB software, you take control of your money. It’s these rules that have enabled me to become a millionaire in less than ten years.

The 4 rules of the YNAB method are:

- Give each of your Swiss francs a job

- Embrace your true expenses

- Roll with the punches

- Age your money (aka Live on last month’s income)

Is the YNAB app free?

No, the YNAB budgeting app is a paid app. It costs 9.08 USD (~ CHF 8.17) if you pay for it annually, or 14.99 USD if you pay it monthly.

But you can trial YNAB for 34 days for free without having to make any commitments.

And you are eligible for a free trial for 1 whole year if you’re a university student (anywhere in the world, including in Switzerland).

Is my data secure with YNAB?

Yes, your data is secure with “You Need A Budget”.

I have my entire financial life (my accounts, transactions, etc.) with them, so I looked into this point thoroughly before choosing them.

Everything is encrypted with YNAB: both the transfer of your data from your computer (or your cellphone) to YNAB services, as well as the data stored on their server. You can read all the geeky details on their “YNAB security page”.

Conclusion

YNAB is currently the best budget app for managing all my assets.

More than being the best, it has become indispensable. Because thanks to YNAB, I have a macro view of my entire financial life (bank accounts, cash, crypto accounts, brokerage accounts, mortgages, P2P loans, properties, my companies’ accounts, etc.)

Mrs. MP and I don’t make any money-related decision without consulting our YNAB.

After more than a decade of using it, I’m still a huge fan of this famous YNAB method which has enabled me to take control of my money (and not vice versa). And as a result, to get a bit closer every day to my dream of financial independence <3

Oh yes, YNAB is not free. But as I often say, it's an investment rather than an expense for me. I can only recommend that you try it out in order to form your own opinion. If you use this link to create your YNAB trial, you'll be supporting the blog, which will earn a small commission, and it makes no difference to you (thanks in advance).