Bank WIR referral code 2025

Bank WIR doesn't offer any promotional codes as such. But if you want to support the blog, you can use my Bank WIR partner link below, and start making big savings on your banking fees thanks to the Bankpaket top:

I’ve been aware of Bank WIR since 2017. At the time, VIAC was launching its 3rd pillar backed by this financial institution.

It isn’t (yet) my main bank for my joint account with Mrs P, but it could become so soon.

Summary of my Bankpaket top review

In short, here’s my opinion of Bank WIR, starting with the advantages of its Bankpaket top:

What I like about Bank WIR’s banking services

- A Swiss bank for Swiss people, established in 1934. It is therefore a “proper official Swiss bank” that is secure and trustworthy and which protects your account up to CHF 100'000 thanks to the Swiss deposit guarantee (which is not the case for all neobanks in the Swiss banking sector — see the alternatives further down in this article)

- Free bank account in Switzerland — with unbeatable conditions: no hidden annual base fees, no exchange rate supplement on payments in foreign currencies with the Debit Mastercard, nor on payments abroad

- One single bank card (the Debit Mastercard) for all my international payments in foreign currencies (online or abroad) without any markup on the exchange rate!

- 24 free Bancomat (ATM) withdrawals per year worldwide, with the last part of the phrase being important: worldwide! I think it’s really practical that the limit is on an annual basis rather than monthly, especially for withdrawing cash once or twice for all the summer vacations abroad

- Digital banking platform to current standards: fully online account creation, self-service payment by bank transfer in the Bank WIR mobile app, no daily transaction limit that is too low (with validation by telephone or whatever!), etc.

- Free joint accounts (!) as well as free partner bank card, so that you and your partner can manage joint household finances in one place, with each having their own Debit Mastercard — for free!

What could Bank WIR improve in the future?

- Simplify the user experience further without the need to install three (!) mobile apps. Currently, you have the Bank WIR app for mobile banking. And you need the Airlock 2FA mobile app for authentication (the first time only), and the free debiX+ app from SIX in order to receive push notifications for your Debit Mastercard. That’s way too many, even if it’s fine once they’re installed

- Low-cost foreign transfers either through Bank WIR doing some work on its fees, or integration with Wise like neon has done

- Swiss cross-border daily account so that cross-border workers can open a Bankpaket top account (currently, a residential address in Switzerland is required in order to be able to open a Bankpaket top account)

- Better integration under the same “roof” of Bank WIR financial products, such as the VIAC 3rd pillar and VIAC mortgage. It would be great if either VIAC or Bank WIR were to be consolidated into one single entity to be even stronger as a Swiss financial institution (a sort of one-stop shop for all personal finance needs)

MP Recommendation

I recommend the Bankpaket top from Bank WIR for their joint account (rather than neon duo). For a private individual, I consider the Bankpaket top to be the second-best bank account behind the neon free account.

Bank WIR’s “Bankpaket top” offering is the cheapest and most comprehensive for a joint account, among all those from the other Swiss digital banks. Furthermore, the Bank WIR app is secure both technologically (a better UX would be welcome in order not to have to install two apps at the beginning), and financially with its total capital ratio of 16.1% in 2024 (compared to the minimum required by FINMA: 10.5% minimum for local banks, and 12.8% for standard international banks).

Since the launch of the Bankpaket top in 2024, I’ve recommended Bank WIR for any Swiss person who is looking for THE best joint account. I don’t use it myself (yet) for the reasons set out in the FAQ of this article.

PS: however, I’m soon going to replace my secondary bank (Zak) with the Bank WIR Bankpaket top (as neon is still a completely online bank, and because the internet can sometimes go down, so I like to have a plan B).

My experience with Bank WIR

At the end of summer 2022, I found myself with a contract signed with Bank WIR. And an enormous smile on my face! Yet I wasn’t aware of them (or only by name) five years earlier.

As I mentioned above, I came across them in 2017, when Bank WIR backed the startup VIAC. This young startup would then go on to become the major key player in 3rd pillars in Switzerland.

And one fine day in 2022, VIAC brought out its mortgage (one of the best, if not THE best). This financial product is backed by Bank WIR.

At the time, I had my 3rd pillar linked to a life insurance policy (big mistake!) which was locked in as collateral with my mortgage with an insurance company (2nd big mistake…). But through perseverance, I managed to get out of these two combined scams by leaving behind several tens of thousands of Swiss francs. But this loss would be compensated for by recovering the missed opportunity cost.

From the moment I realized that my insurer was folding and could no longer put up with me contacting them every week, I got in touch with VIAC and Bank WIR in order to obtain a product that is actually focused on the customer (and not on the banker’s bonus!).

And that’s how Bank WIR became synonymous in my eyes with satisfaction, smile and professionalism.

Why is Bank WIR the best Swiss bank for a joint account?

Bank WIR (with its Bankpaket top) is the cheapest bank for the daily needs of couples, partners or roommates who are resident in Switzerland and have a Mustachian mindset. From their financial solidity, to their 100% free joint account with a free Debit Mastercard per partner (with the lowest fees for foreign currency transactions and payments abroad), the Bankpaket top is simply the most optimal (and available via secure online banking and mobile banking that meet Swiss security requirements).

The Mustachian criteria for choosing your Swiss bank for your frugal joint account

In practical terms, here are the criteria on which I judge which is the Mustachian bank that offers the best joint account in Switzerland.

It must meet these quality standards:

| Criteria | Bank WIR (Bankpaket top) | Comments |

|---|---|---|

| Account fees | Free | No base fees. |

| Mobile and digital bank | ✅ | |

| Secure | ✅ | Regulated by FINMA, data stored in Switzerland, and two factor authentication for online banking. |

| Free transfers within Switzerland | ✅ | |

| Free transfers in Europe | ✅ | Via SEPA transfers (no transaction fees, but surcharge on the exchange rate). |

| Inexpensive international transfers | ❌ | Neon is better with Wise integrated in their mobile app. |

| Free debit card | ✅ | A free one for each partner! |

| No foreign currency payment surcharge | ✅ | Better exchange rate applied (Bank WIR better than neon on this point) |

| Free withdrawals from ATMs | ✅ (24x / year) | Big bonus: these withdrawals are also free abroad! |

| Free money deposits | 🟠 (via TWINT) | |

| QR bill payment by scanning | ✅ | |

| Supports eBill | ✅ | |

| Statements in CSV format | ✅ | Perfect for synchronizing your transactions with the budget app YNAB. |

| Statements in PDF format | ✅ | |

| Push notifications | ✅ (via SMS) | |

| Mobile payment methods | ✅ | Apple Pay, Google Pay, Samsung Pay, Garmin and Fitbit. |

| Available in FR / DE / EN / IT | ❌ (FR, DE, IT) | No English. |

| Bonus: physical access | ✅ |

Thanks to its mobile app, Debit Mastercard and digital banking platform built on its solid foundation that has existed since 1934 (!), the Bank WIR Bankpaket top fulfills all the conditions for a Swiss joint account, with the exception of:

- “Inexpensive international transfers” — but there’s a readily available solution: you just need to create a Wise account to get the cheapest international transfer fees on the market. It’s a bit less practical than neon which integrates this in its app, but for the few times I’ve used it, it works.

In sum, Bank WIR offers the best joint account in Switzerland with its Bankpaket top.

PS: Bank WIR doesn’t have an annoying daily payment limit of 5'000 CHF (or 25'000 CHF or 50'000 CHF per week), as can be the case with neon or Zak. Even if I don’t need to transfer such amounts every day, this type of freedom can be much more practical rather than having to contact customer support to release a payment.

Reviews by WIR bank account users

Like any self-respecting Mustachian, before choosing something as important as the place where my salary and savings are held, I consult several opinions online.

I’m therefore going to make your job easier by compiling some screenshots (from March 2025).

Average ratings for the Bank WIR mobile app in app stores

Firstly, you’ll find below the average ratings from reviews of the Bank WIR app in the iOS and Android app stores:

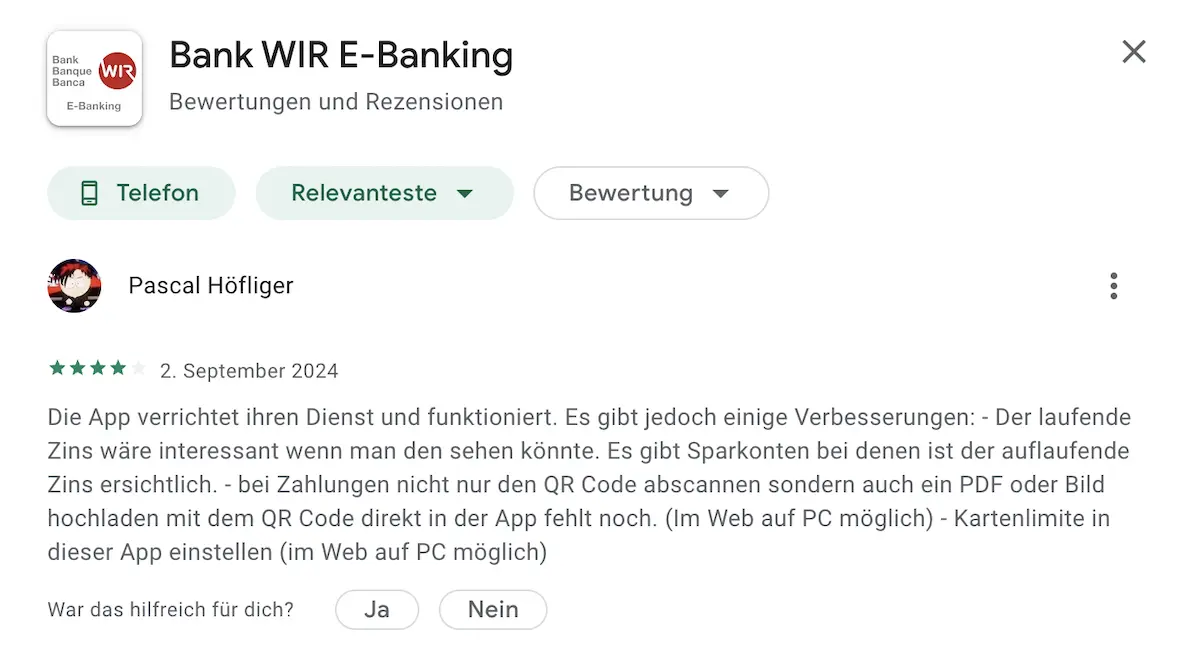

Comments about the Bank WIR mobile app on app stores

And here are some public comments from Bank WIR users on the Apple AppStore and the Google Play Store:

The majority of negative comments come from people who use their cellphone in English, and suddenly the app displays in German. You need to have your phone language set to French in order to view the app in French.

But overall, compared to neon, there are only 20 or so reviews of the Bank WIR app, so I don’t consider this to be sufficiently representative in order to take this as the sole source of truth.

You can also use these links to view the most recent ratings of the iOS Bank WIR app and the Android Bank WIR app depending on your smartphone type.

I also recommend you read this discussion thread on the MP forum about the Bankpaket top.

Alternative solutions to Bank WIR — and how they compare

As a reminder, I’m mainly comparing the Bankpaket top from a joint account perspective, and not a private individual account perspective (as for the latter, neon is the best solution).

neon duo or Bank WIR (“Bankpaket top”)

Bank WIR with its “Bankpaket top” is better than neon duo for a Swiss joint account. This is for three main reasons: free joint account, a free Debit Mastercard for each of the joint account holders, and a better exchange rate applied to foreign currency transactions (online or in shops abroad).

The only two reasons making me stay with neon duo at the moment are: my negotiating power (I don’t want to have my VIAC mortgage with Bank WIR AND my entire my banking relationship, so that I’m not 100% tied to a single bank), and supporting the very first Swiss neobank (a purely and unusually emotional reason with these CHF 6/month that I view as my support for the development of neon Bank).

Zak vs Bank WIR

Zak doesn’t offer a joint account as such. You and your partner can create a Zak account each, and use their pot system.

But Bank WIR’s Bankpaket top offers a proper Swiss joint account, so it’s better than Zak.

If you’re looking for a mobile bank for your personal needs (you don’t require a joint account), then Zak is a good alternative (see my detailed analysis of the best Swiss bank here).

Bank WIR vs Revolut

Revolut is not a proper Swiss bank. This neobank doesn’t hold a banking license in its own right — neither in Switzerland nor anywhere else. It is only an e-money institution (aka fintech). This means it is required to hold your money in a third-party bank. Whereas Bank WIR is a proper bank with a Swiss banking license.

Typically, a major shortcoming of Revolut is, for example, the absence of the Swiss eBill payment method. With Bank WIR, you can pay these eBills.

When it comes to the Revolut card, it’s one of the cheapest ways of managing currencies and payments abroad (i.e. very low exchange rate markup). But there again, Bank WIR has made a great move with its Debit Mastercard which is cheap for foreign currency payments.

Personally, I don’t use Revolut anymore. The Bankpaket top is better both for banking services and foreign currency payments.

Bank WIR vs Yuh

Yuh is a digital bank which uses a third-party bank (Swissquote) for its banking infrastructure. Swissquote is regulated by FINMA, so your money is protected up to 100'000 CHF. Yuh is a good competitor to the Bankpaket top with its free account, but remains some way behind with its high currency exchange fees (0.95%!)

In addition to their banking services, Yuh is also active in the investment sector. But similarly, their management fees are too high compared to other investment alternatives available for Swiss Mustachians.

In my opinion, Yuh has spread itself across too many initiatives (bank, foreign currency, investment, crypto), and is therefore not optimal enough in any of them.

In summary: Bank WIR’s Bankpaket top remains better than Yuh for my banking and payment needs.

ZKB Banking vs Bankpaket top (Bank WIR)

The Zürich cantonal bank also offers a free joint account. The package is called “ZKB Banking” which also includes a free debit card, as well as TWINT and the usual online banking platforms. However, the fees for foreign currency transactions are high (1.25%) compared to the Bankpaket top.

Another big negative point for some Swiss people: ZKB Banking is only available in German (not in French, and the English version is not great).

Bank WIR’s Bankpaket top is still less expensive for foreign currency payments (compared to ZKB Banking which applies a surcharge for foreign currency payments).

Bank WIR vs N26

N26 is a mobile bank based in Germany. Its clients’ assets are protected up to 100'000 € under the German deposit protection system. Their N26 joint account is free, and also comes with a virtual Mastercard debit card. The problem is that the N26 account is in euros, and has a German IBAN.

N26 still doesn’t have a Swiss IBAN, so you can’t pay in your salary in Swiss francs to N26. And as with Revolut, N26 doesn’t offer QR bill payment.

So let’s not waste time comparing apples with oranges, as Bank WIR easily wins over the German fintech.

Bank WIR vs Migros Bank

Migros Bank is a traditional Swiss bank, one of the cheapest on the Swiss market. Like Bank WIR, it’s an “official bank” with a physical presence. Migros Bank offers free account management if you maintain a balance of at least CHF 7'500 Swiss francs. But it can’t compete with the Bankpaket top on currency exchange transaction fees.

Due to Migros Bank’s expensive exchange fees, the Bankpaket top from Bank WIR remains much more advantageous.

Bank WIR or Alpian

Alpian is a private online bank. It also offers investment services. However, being a premium bank also means premium management fees (minimum 0.75% investment mandate fees). Furthermore, Alpian doesn’t offer a joint account.

In addition to being much more expensive than Bank WIR (and the other Mustachian online trading platform options), Alpian is not comparable with the Bankpaket top because this private bank doesn’t offer a joint account.

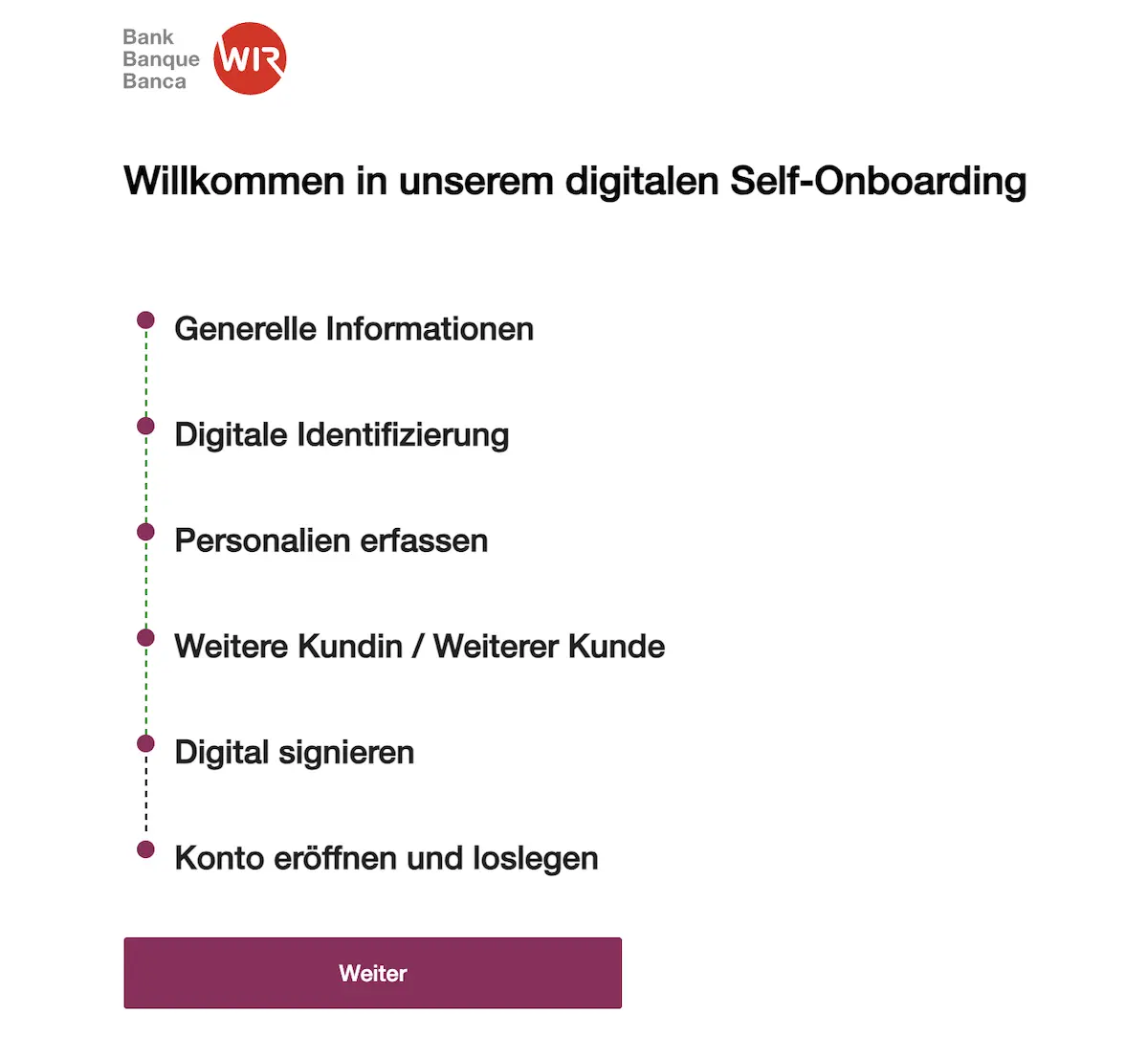

Open a WIR account in 10 minutes

The account opening procedure is very simple, so there’s no need for me to show you detailed screenshots.

The entire 6-step process is digitized via the Bank WIR website, and only takes 10 minutes:

- Fill in your general information

- Confirm your identity via digital identification

- Input your personal details

- Add your partner’s information (additional customer)

- Sign online in a completely digital manner

- Your bank account is open, you’re in!

FAQ about the Bankpaket top

Who manages Bank WIR?

Bank WIR was founded in 1934. Suffice to say their internal processes are well established, including the manner in which they’re structured.

You can see the composition of Bank WIR’s senior management via this link, and the members of the board here. I’ve looked at the profile of all these people and it’s reassuring: experience, seniority and expertise are the keywords.

Is Bank WIR a secure bank?

Yes, Bank WIR is secure. It holds a Swiss banking license. It is subject to the strict FINMA regulations. Your money held in a “Bankpaket top” joint account is therefore protected up to 100'000 CHF under the Swiss deposit guarantee.

Another point proving Bank WIR’s financial solidity: its total capital ratio is 16.1% (2024 figures), while other banks stick to the minimum required by FINMA (meaning 10.5%).

Is Bank WIR a bank?

Yes, Bank WIR is a proper Swiss bank, with a banking license from FINMA. It has been so since 1934.

What is the Bankpaket top?

The Bankpaket top is the everyday banking solution from Bank WIR. It’s an all-in-one solution: private account with IBAN in CHF so it can accept your Swiss salary, QR bill payment, Debit Mastercard which can be used fee-free worldwide, uses TWINT.

And the best thing is that this Bankpaket top is available for joint accounts!

Which accounts does Bank WIR offer?

Bank WIR offers the following bank accounts:

- Bankpaket top: free and with excellent conditions

- Beteiligungs-Sparkonto: for long-term savings

- Sparkonto: more interest and with full flexibility

- Sparkonto 60+: savings account for retirement

- unyt Konto: product based on Bank WIR’s new digital currency (limited to the Basel region)

- CHF-Kontokorrent: the predecessor of the Bankpaket top, which I think will soon disappear

- It also offers business accounts (including the KMU-Paket for SMEs)

Graphical overview:

Eligibility conditions for opening a Bankpaket top

You must satisfy one (minimum) of the following conditions to be able to open a “Bankpaket top” account with Bank WIR:

- Regularly pay in an amount of CHF 1'500 (easy if you use it for you or your partner’s salary payment)

- Retirement fund of a minimum amount of CHF 20'000 with Bank WIR (VIAC 3a account doesn’t works here, as we’re talking about a Terzo account here)

- A mortgage of at least CHF 300'000 with Bank WIR

- Hold a membership share in Bank WIR (CHF 200)

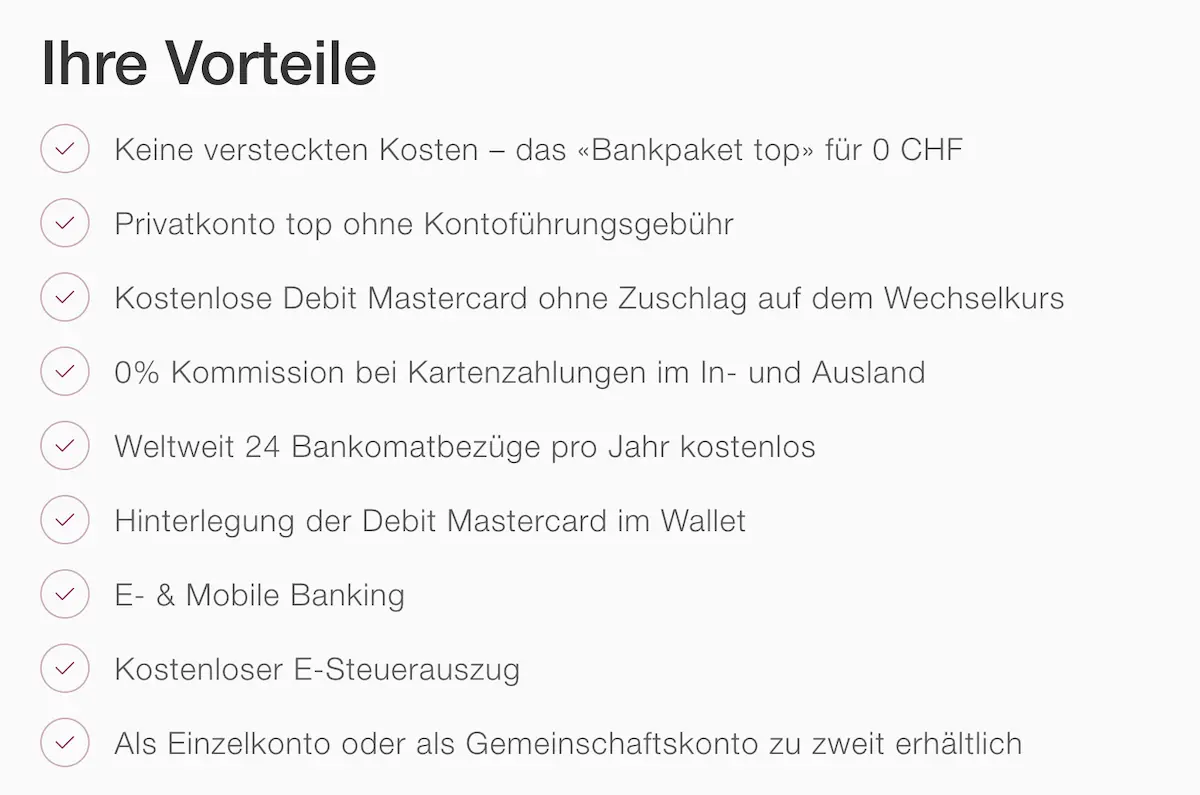

Is the Bankpaket top totally free?

For your daily banking operations, yes, Bank WIR’s Bankpaket top is totally free. No hidden fees like in other traditional banks, or unjustified additional card fees for paying in a foreign currency. Likewise, all bank transfers in Switzerland are free, as well as domestic payments in CHF.

When it comes to Bankpaket top services that have a fee, here are Bank WIR’s fees:

Bankpaket top fees in Switzerland 🇨🇭:

- You get 24 free ATM withdrawals per year, then you have to pay a withdrawal fee of CHF 2 for each additional withdrawal

- If you want to receive documents in paper format (rather than electronic), you’ll have to pay CHF 2 per package

Bankpaket top fees abroad ✈️:

- When you make payments in a foreign currency abroad (or online) with your WIR debit card, an exchange rate that is more favorable than the average Mastercard rate is applied — and this is without a surcharge on the interbank rate, which saves you several hundreds of francs per year if you do some traveling outside Switzerland

- If you make electronic transfers in foreign currencies (outside the SEPA area), fees of CHF 5 per transaction are charged

Does Bank WIR offer a joint account?

Yes! Bank WIR offers its “Bankpaket top” in the form of a joint account, and without any surcharge! Their joint account is free. You’ll find all the useful information about the Bankpaket top (joint account) via this link.

Is there a maximum wire transfer amount per day or per week with the Bankpaket top?

No, it has no limit. In the sense that it is the credit balance of the account that primarily determines the limit.

Is there an upper limit for card payments?

The Bankpaket top card comes with a standard daily limit of CHF 3'000 and a monthly limit of CHF 15'000, which can also be adjusted (upwards or downwards) via Bank WIR’s e-banking.

Should I use Bank WIR for my daily banking activities?

The Bankpaket top is the best joint account in Switzerland if you’re a Mustachian. Its personal account for two partners is the cheapest and enables you to save a lot on banking fees. These savings can then be invested in the stock market in order to make them grow — for you, not for your banker’s bonus!

Can I have my salary paid into Bank WIR?

Yes, you can. Bank WIR (through its Bankpaket top) provides you with a Swiss IBAN. You can therefore receive your salary in Swiss francs (CHF).

This is actually one of the big advantages compared to N26 which only offers a German IBAN. But a Swiss IBAN is necessary in order to receive your salary without any issues with your Swiss employer (and without being subject to exchange rate fluctuations from a foreign IBAN).

Should I pay my salary into my WIR account?

Bank WIR is a reputable and reliable Swiss bank. It has existed since 1934. Also, your money is protected up to CHF 100'000 under the Swiss deposit guarantee.

Conclusion on the WIR joint account

Bank WIR is a very good financial institution. It offers the best joint account for us Swiss Mustachians.

Since 2024, the “Bankpaket top” is the one that I recommend if you’re looking for a joint account.

With this free package, you can pay all your bills (via eBill or QR-bill!), and make your national transfers in CHF through the WIR Mobile Banking app.

The Debit Mastercard from Bank WIR is the best on the market for withdrawing money from ATMs for free, and for paying in shops when credit cards aren’t accepted (see my strategy for bank cards in this article.

When you’re abroad, the Bank WIR payment card is the only one you’ll need for all your purchases in foreign currencies.

The same for online payments: you can also use it for payments in foreign currencies in order to pay the lowest amount in exchange fees (and you can use your Swiss credit cards for online payments in CHF in order to maximize your cashback).

The few negative opinions (app in German if your cellphone is in English, and fees of CHF 15 for closing the account) are negligeable to my mind.

In sum: if you’re looking for the best joint account in Switzerland, choose the Bankpaket top from Bank WIR.