While Swiss fintechs have certainly shaken things up in the outdated world of Swiss personal bank accounts… they’ve not been in a hurry to bring out a decent joint account…

Well, that was until 2022-2023…

And what if it were now possible to find an attractive Swiss joint account in terms of account fees and debit card (just like for personal accounts)?

What is a joint account?

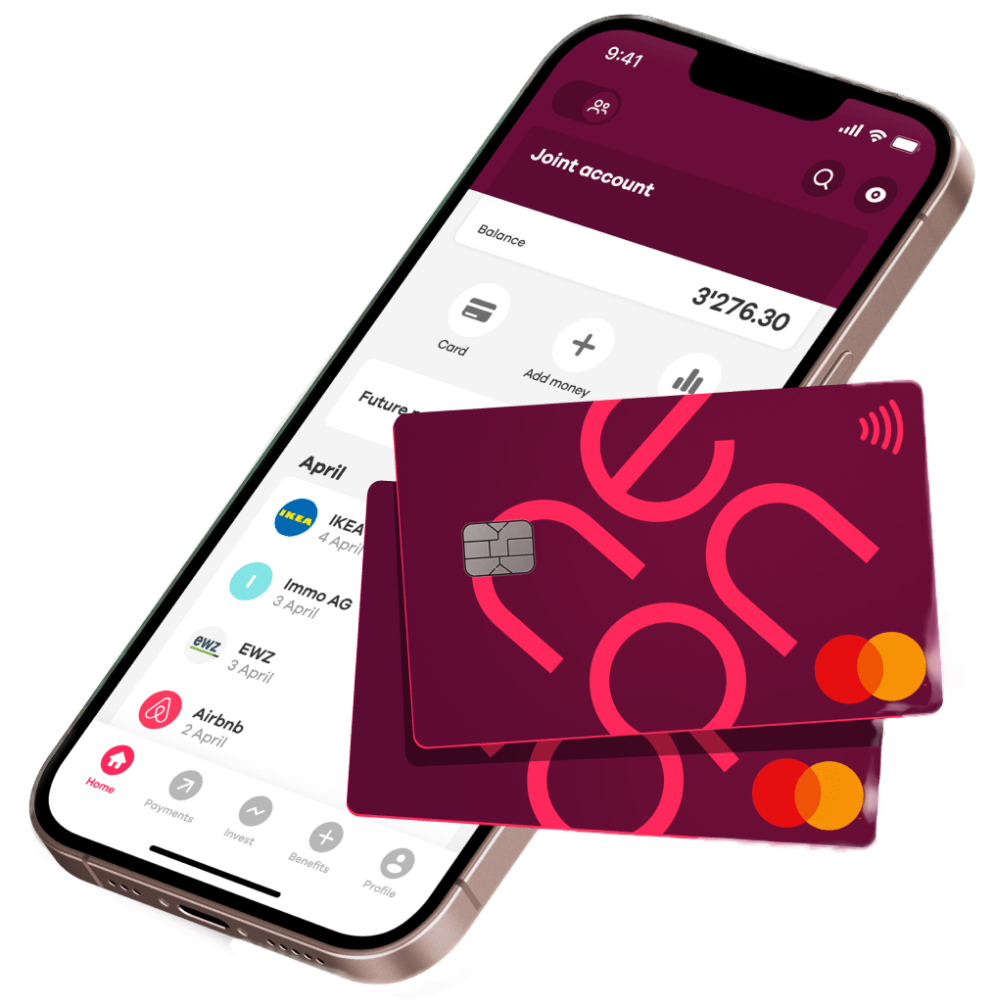

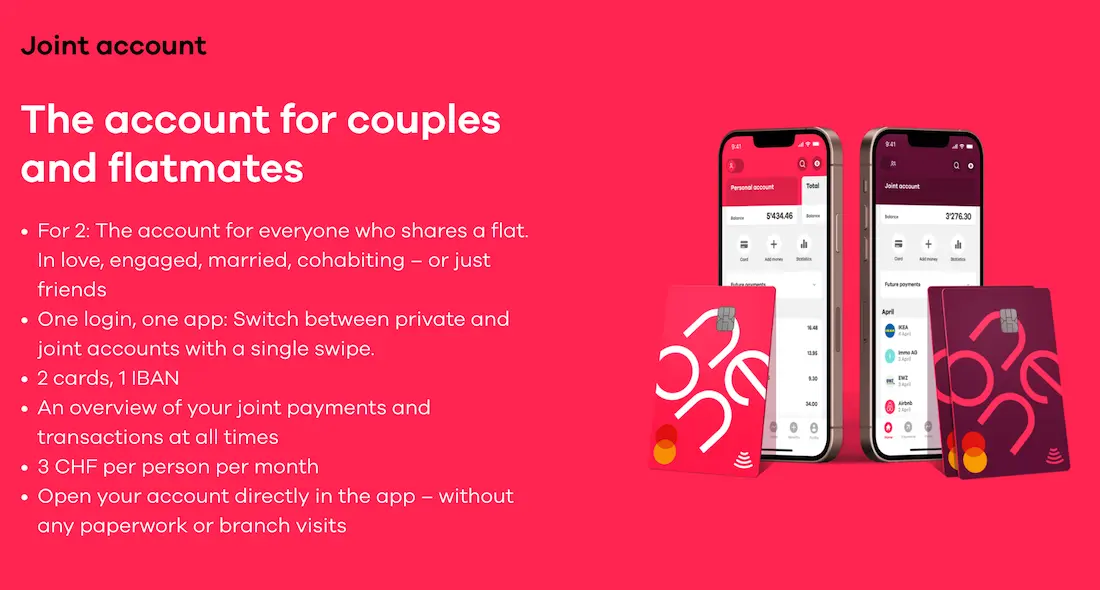

A joint account, also called shared account, is a bank account shared between two (or several) people, often couples (married or civil partnership) or roommates. Each account holder has equal access to manage the joint finances, so it is therefore vital to have good trust and communication between joint account holders.

What is a joint account for?

First, the politically correct response: one of the main benefits of joint accounts is to combine the income of several people, in order to pay shared day-to-day bills (rent, electricity, etc.) that you owe jointly with the other account holder (partner or roommate).

Opening a joint account enables you to have access to joint funds without having to transfer money between different individual bank accounts…

In my case, the non-politically correct response: to be legal. Until October 2024, Mrs MP and I used a single individual bank account in one of our names. We paid both our salaries into it and all our expenses out of this personal bank account.

However, … a Swiss personal bank account must only contain money that comes from the beneficial owner. And as the Swiss banking ecosystem (as well as the international one) is coming under tighter control, we had to prove every month that one of the salaries coming into this bank account belonged to another beneficial owner… It was the same for all the payments made to the other person…

So, it was becoming a hassle to prove everything, AND in addition it wasn’t strictly legal.

Mrs MP and I therefore decided to open a joint account.

Criteria for finding the best joint account

So, I outlined all the Mustachian criteria to determine how joint accounts work for us, helping to compare options and select the most cost-effective one:

- No fees or charges incurred in holding a joint account

- Mobile and digital banking

- Secure

- Free transfers within Switzerland

- Free transfers within the eurozone (via SEPA)

- Low international transfer fees

- Free debit card

- No surcharges for foreign currency payments (online or abroad)

- Free cash withdrawals at ATMs

- Free cash deposits

- Payment of QR bills by scanning

- Supports eBill

- Downloadable account statements in CSV format (for synchronization with YNAB)

- Downloadable account statements in PDF format

- Real-time push notifications

- Mobile payment methods (Apple Pay and Google Pay at the very least)

- Available in FR / DE / EN / IT

- Bonus: in-person access in the event of IT issues

Comparison of the best joint accounts

After comparing all the joint accounts available in Switzerland, I came up with the following shortlist:

Bank WIR (“Top banking package”):

Zurich Cantonal Bank (“ZKB Banking” package):

neon bank (“neon duo” package):

Before analyzing joint accounts in detail, I’ll explain the works, benefits, and pitfalls of joint accounts and why I didn’t shortlist the following banks:

- Zak: doesn’t offer a joint account as such

- Migros Bank: CHF 30/year for the second card of one of the two account holders…

- Raiffeisen: only free for members (between CHF 200 and CHF 500 depending on the Raiffeisen bank)

- PostFinance: CHF 5/month

- UBS: CHF 9/month

- All the cantonal banks: more than CHF 3/month and/or debit card with an annual fee, and only free with a minimum deposit, according to Moneyland (see the next point below)

- Except the Aargau Cantonal Bank (worth looking at if you live in the region)

And so, here is my comparison of joint accounts:

| Criteria | Bank WIR | ZKB | neon duo |

|---|---|---|---|

| Account fee | Free | Free | CHF 6 / month |

| Mobile and digital banking | ✅ | ✅ | ✅ |

| Secure | ✅ | ✅ | ✅ |

| Free transfers within Switzerland | ✅ | ✅ | ✅ |

| Free transfers within Europe | ✅ | ✅ | ✅ |

| Low-cost international transfers | ❌ | ❌ | ✅ (via integration with Wise) |

| Free debit card | ✅ | ✅ | ❌ (CHF 10 / card) |

| No foreign currency surcharges | ✅ | ❌ | ✅ |

| Free ATM withdrawals | ✅ (2x / month) | 🟠 (only ZKB) | ✅ (3x / month) |

| Free to pay in money | 🟠 (via TWINT) | ✅ (only ZKB) | 🟠 (via TWINT) |

| QR bill payment by scanning | ✅ | ✅ | ✅ |

| Supports eBill | ✅ | ✅ | ✅ |

| Statements in CSV format | ✅ | ✅ | ✅ |

| Statements in PDF format | ✅ | ✅ | ✅ |

| Push notifications | ✅ (via SMS) | ✅ | ✅ |

| Mobile payment methods | ✅ | ✅ | ✅ |

| Available in FR / DE / EN / IT | ❌ (DE, FR, IT) | ❌ (DE, EN) | ✅ |

| Bonus: in-person access | ✅ | ✅ (Zurich) | ❌ |

I made the following notes while preparing this joint bank account comparison:

- Bank WIR gets a bonus point for offering 24x free ATM withdrawals (per year) which are valid in Switzerland and also the whole world!

- However, Bank WIR charges CHF 5 per transfer in a foreign currency (except for SEPA Europe)

- Lastly, Bank WIR requires that clients meet one of the following four conditions in order to be eligible for the Top banking package:

- Regular deposit of CHF 1'500 per month (in essence so that you have your salary paid into this account — for info, neither ZKB nor neon duo has a monthly minimum)

- Pension fund of at least CHF 20'000 held with Bank WIR

- A mortgage of at least 300 000 CHF held with Bank WIR (you can easily fulfil this criteria if you hold a VIAC mortgage)

- Hold a share certificate in Bank WIR (one-off payment of CHF 200)

- It’s great to be alive in the 2020s when you realize that these 3 banks (Bank WIR, ZKB and neon) all enable you to create a bank account 100% online!

Soooo… which is the best joint account in Switzerland?

Top 3 rated joint accounts in Switzerland

The result of the comparison is pretty clear: the most frugal place for opening a joint account is WIR Bank’s “Top banking package”.

🥇 This 1st place for Bank WIR is mainly down to these advantages:

- Zero fees for joint account holders

- Free debit card

- Zero fees for foreign currency transactions + application of the interbank rate without any mark-up!

- Free ATM withdrawals (24x/year) worldwide

- Available in German, French, and Italian

🥈 The 2nd best joint account is the “ZKB Banking” package of the Zurich Cantonal Bank. But this joint account may not be handy if you aren’t able to speak German or English, and if you want to use your debit card for foreign currency transactions. If this is not suitable for you, then the second-best joint account is neon duo.

N.B. as reader Juriaan pointed out to me, the English section of the ZKB website is very approximate. There are very often untranslated sections, and this is quite problematic. On the other hand, they’re very responsive by phone, and no problem at all communicating in English.

🥉 The 3rd best joint account goes to neon duo. Their fees of CHF 6/month (and CHF 10 per card) don’t help. But in exchange for that, you get a very useful integration with Wise (in order to be able to make low-cost foreign currency transactions), 36x free withdrawals in Switzerland, and an optimal credit card in terms of fees for foreign currency transactions.

“Zero fees” in exchange for a minimum deposit? Watch out!

Numerous Swiss banks (especially cantonal banks) offer zero fees if you always maintain a certain account balance (CHF 10'000 to CHF 25'000).

Even if you aim to keep a financial cushion of such an amount, you want to make this money work in a savings account or a certificate of deposit (CD, aka “Savings Accounts with Notice Period” in Switzerland) for example (rather than letting your bank keep this potential interest).

To illustrate this in figures, imagine you choose the zero fees of such an account with BCV, the Vaud cantonal bank, you would save 12x their fees of CHF 3.50/month, which is CHF 42.

But if you choose opening a joint account with WIR Bank’s free “Top Banking Package” and place this CHF 15'000 financial cushion into a savings account with a 1% interest rate (elsewhere than at Bank WIR), you could earn CHF 150 annually!

And if you prefer to invest this financial cushion in the stock market in a global ETF (~6%), then we’re talking about savings of CHF 900 which go into your pocket rather than BCV’s :)

So, don’t get taken in by “zero fees” in exchange for a minimum deposit (which just makes the banks richer above all else).

Conclusion

Here’s my final ranking:

Best joint account in Switzerland

- Bank WIR

- ZKB

- neon

It’s nice living in this era of everything being online, where you can open a joint account from your sofa, in less than 10 minutes. Do you remember when you had to make an appointment on the telephone, travel to the bank, wait, sign dozens of documents… no thanks!

By going with Bank WIR’s “Top banking package”, you can be assured of having the lowest fees possible for the best banking conditions (including debit card in CHF and foreign currencies).

And how about you, which joint account have you chosen?

Introductory offer codes

The blog is able to provide you with the following introductory offer codes for each of these joint accounts:

Bank WIR promo code

- Unfortunately, Bank WIR doesn’t offer promo codes as such. If you’d like to support the blog, however, you can use my Bank WIR partner link: click on this link to open your joint Bank WIR account.

neon promo code

- The promo code “neonMustachian” gets you the neon Debit Mastercard for free + a CHF 10 welcome bonus — which must be entered when you sign up as it’s not possible afterwards. (N.B. the app may not reflect the bonus directly, but it’ll be taken into account, I checked with their support)

FAQ

Household account, partner account or joint account?

You can even add “shared account” to the list of synonyms. In Switzerland, all these terms are used to describe a joint account, where the account is a bank solution shared between several people.

I thought there was a Zak joint account too?

Technically, Zak doesn’t offer a joint account in the name of two different joint account holders Their solution consists of two separate personal accounts, and a shared pot system where you can manage joint expenses.

Why do you use neon duo yourself, MP?

At the time of writing this, we use neon duo (more details in this article) in the MP family.

Surprising? Well, it’s because this is one of the rare occasions when my personal opinion differs from the most frugal. My two reasons for choosing neon duo are:

- Negotiating power: I already have my VIAC mortgage with WIR Bank, and I’ve always wanted to be careful not to be 100% tied to one single bank, in order to maintain my negotiating power. Although I took out my VIAC mortgage with them without needing to do any negotiating. But anyway… I’ll let you know if I change my mind one day.

- Supporting the very first neobank: The second reason is (unusually) emotional. As a joint account holder, I see these CHF 6/month as my way of supporting the development of neon bank, which dared to challenge outdated and exploitative Swiss institutions.

But, if you’re looking for the most frugal joint account, and these two points don’t really matter to you, then objectively, I recommend you choose Bank WIR’s “Top banking package”.