I discovered the concept of vested benefits for the first time when I changed job.

I’d received a letter from my 2nd pillar which asked me what I wanted to do with my assets: transfer into the pension fund or into a vested benefits account.

In short, when you leave a job or go to work abroad, you have to “store” your occupational pension fund assets (the oft-mentioned 2nd pillar) in an account called “vested benefits”.

But as usual, you have several options available to you with sharks who are waiting to siphon off your money through astronomical fees, making your savings melt away like snow in the sun.

So here’s my simple and practical guide to help you make the right choice.

What is a vested benefits account?

A vested benefits (also referred to as earned benefits, secured benefits or non-forfeitable benefits) account enables insured persons to store your previous pension fund savings (2nd pillar) when:

- You leave your job without going directly into another one (career break between two jobs, unemployment, sabbatical, training, parental leave)

- You go to work abroad

- You become self-employed (freelance work), without withdrawing your 2nd pillar assets to fund your new project

- You earn less than the minimum threshold for LPP (occupational pension fund) contributions (like a 10% job)

- You get divorced and receive a portion of your ex-partner’s assets

All this money from your occupational pension fund therefore remains locked away in such a vested benefits account until you find a job with a wage subject to the 2nd pillar, you move abroad permanently, you buy your main residence (EPL, for “Encouragement à la propriété du logement” in French, “encouragement of home ownership” in English), or you use your existing retirement assets for their intended purpose whem the time comes: retirement.

What types of vested benefits accounts are there?

Just like for the 3rd pillar (also known as pillar 3a), there are different ways to store your new pension fund money in vested benefits:

- Vested benefits account in a bank with guaranteed interest (a bit like a savings account)

- Vested benefits policy linked to life insurance (cover in case of death or incapacity)

- Digital vested benefits account invested in the stock market

If you’re familiar with the subject of pillar 3a, you’ll notice that they are more or less the same options.

As a Mustachian AND when you’re at the stage of building your wealth (i.e. you’re not yet financially independent), we want to make our money work to the maximum.

Which essentially means:

- Vested benefits accounts (aka earned benefits accounts) with banks generate much too little, like the BCV vested benefits account (around 0.01% interest rate at the absolute maximum, depending on the BNS base rate)

- Vested benefits (aka earned benefits) with insurance companies are as opaque as the 3a linked to life insurance (what a great legalized scam!)

- The only remaining viable option: the vested benefits accounts that you can invest in the stock market with the maximum possible in stocks, such as finpension and VIAC

Is it really beneficial to optimize the vested benefits allowance?

Let’s imagine that you have CHF 120'000 in LPP, and you leave your job for 15 years (long sabbatical, decide to be an entrepreneur, or simply FIRE).

Taking into account compound interest, you’ll end up with:

| Bank (1% interest) | Option invested in the stock market (7% return) | |

|---|---|---|

| Initial non-forfeitable benefits amount (in CHF) | 120'000 | 120'000 |

| Vested benefits amount in 15 years (in CHF) | 139'323 | 331'095 |

| Difference in favor of a stock market option | +191'772 |

So yes, it’s very beneficial to optimize your secured benefits. We’re not talking about several tens or hundreds of Swiss francs, but in fact several hundreds of thousands of CHF!

Criteria for making a good choice of vested benefits account

I’ll remind newcomers that, on this blog, we want to make our money work while we’re sleeping.

This is in order to be able to live off these returns.

The first piece of good news: we can invest the money from our vested benefits occupational pension in the stock market!

And the second piece of good news: new players are offering options that are 100% online with much lower fees than banks (like the BCV vested benefits foundation) or insurance companies. And that’s good for our wallet!

And so here are the Mustachian criteria to follow in order to choose the best earned benefits option:

- 100% in global stocks

Look for the option that allows you to invest the maximum possible in global stocks. Effectively, these stocks cover the whole world and provide you with an optimal return-risk ratio through their wide diversification. - Passive investing

In case a reminder is needed: you want to invest passively, and not via a banker who dabbles in the stock market. Why? Because, time and time again, scientific papers prove that over an investment period of 10 years or longer, passively managed funds beat actively managed funds. - Two earned benefits foundations

In order to optimize your tax position, it’s legal to withdraw your 2nd pillar retirement savings over two different tax years. This then enables you to prevent progressive taxation via a phased withdrawal (cool to reduce your tax liability during the transition period). In order to use this strategy, you need an earned benefits provider that has two earned benefits foundations (as you can’t have two portfolios with the same foundation, that you would withdraw over two different tax years). - The best return

You want the earned benefits option offering the best return, once all the fees have been deducted. Because after all, it’s for this return that you invest in the first place. - Most favorable tax domicile

This is particularly important for expats. If you withdraw your vested benefits when you move abroad, and only in this case, the location of your vested benefits company is the determining factor when it comes to withholding tax on lump-sum pension benefits. So it’s in your interest to find a pension fund located in the most tax-efficient canton.

IMPORTANT REMINDER: never take out a secured benefits option with an insurance company!!!

Just as I repeat for 3a mixed insurance, the same goes for secured benefits pension fund: NEVER put your pension assets with an insurance company.

Their products are sub-optimal: you get little return, but they get rich with big fat bonuses.

If you want to take out life insurance or loss of earnings insurance, that’s perfectly legitimate. But in this case, you need to take out these two products separately:

- Non-forfeitable benefits with a company (see below)

- “Pure” life insurance / incapacity insurance / loss of earnings insurance, meaning that it only covers that. I recommend that you read my article specifically on this subject of the best life insurance in Switzerland

Candidates for the best non-forfeitable benefits product in 2026

Until 2018, you only had the choice between so-so earned benefits products (those from banks) and lousy products (those from insurance companies).

Fortunately, finpension came along and shook things up with a 100% online earned benefits product in 2018. And VIAC followed with its own offering in 2020.

Frankly, it’s great to be living in such a time, where you have high-quality financial products, and which optimize your return for you as a client!

Currently, the only two worthwhile competitors for secured benefits are:

And here is how these two financial institutions compare with regard to our Mustachian criteria:

1. Invest 100% of the non-forfeitable benefits in global stocks

The devil is in the detail, as both finpension and VIAC offer “100% global stocks” strategies.

But for VIAC, you can only use their “Global 100” strategy for the non-compulsory part of your LPP… whereas with finpension, you can use their “Actions 100” strategy for all your secured benefits (compulsory part AND non-compulsory part).

The compulsory part covers your salary between CHF 22'680 and CHF 90'720 (in 2026) in order to guarantee you a minimum pension, or help in the event of incapacity or death.

The non-compulsory part is the bonus: everything above the legal minimum. Your employer can provide a higher salary or offer better benefits, depending on the occupational pension plan. The higher it is, the better it is for your retirement!

With this information, finpension comes out as a clear winner on this point.

Especially when you add to this point that VIAC imposes a maximum amount of 60% invested in foreign currencies (in addition to CHF), while finpension allows you to invest up to 99% without any problems.

2. Passive investing

On this point, finpension and VIAC are equal. Both of them use passively managed indexed investment funds. These funds are accessible to institutional investors who have enormous amounts under management, which is the case here. This is great as indexed funds are even more advantageous than ETFs in terms of fees!

The strategies offered are also proven. The one that interests us, with 100% in stocks, is more or less the same between VIAC and finpension.

3. Two secured benefits foundations

The current law allows you to withdraw your earned benefits over two occasions in two different tax years. That therefore enables you to prevent progressive taxation via a phased withdrawal.

BUT, you can’t withdraw your secured benefits twice…

It’s for exactly that reason that a certain finpension got ahead of the curve by offering two foundations to its clients (more info on this subject in this finpension article on splitting secured benefits).

VIAC currently only offers one foundation.

finpension therefore comes out on top on this point, which can save you several thousands or even tens of thousands of Swiss francs in tax, depending on which canton you live in.

4. The best return

As for the 3rd pillar, I now focus on the best return rather than the lowest fees. Because, in the end, it’s the total net return that’s important.

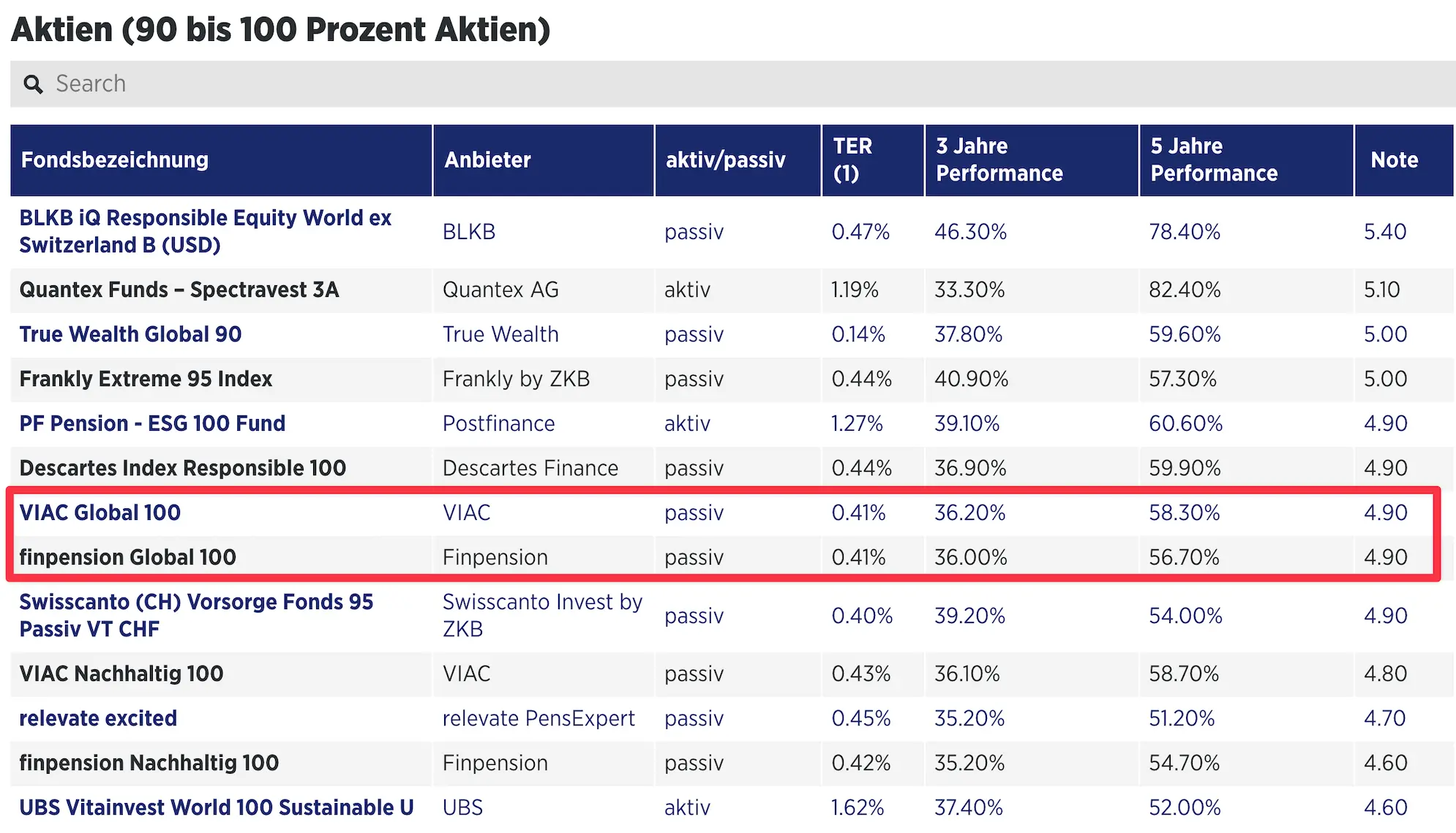

For this, I use the Handelszeitung (a Swiss German economic newspaper) ranking compiled by the Haute École de Gestion de Fribourg.

Basically, with both finpension and VIAC, the composition of the “100% global stocks” strategy is the same for pillar 3a as for vested benefits.

Looking at the performance over the last 5 years (finpension = 37.20%, VIAC = 36.90%), we can therefore say that finpension and VIAC are pretty much on an equal footing.

However, the fees are different between the 3a and earned benefits:

- finpension: 0.49%

- VIAC: 0.43% (= 0.41% + 0.02% foreign currency fees)

With a difference of 0.06%, on secured benefits of CHF 500'000 for example, we’re therefore talking about CHF 300 in favor of VIAC.

Based on this, I should therefore tell you: “VIAC is better for secured benefits as it has lower fees than finpension!”

Yes, BUT…

I must remind you that VIAC only allows you to invest the non-compulsory part of your secured benefits in a “100% global stocks” strategy…

So the CHF 300 saved on the fees of a VIAC portfolio are largely outweighed by the return on the compulsory part that is 100% in stocks in a finpension portfolio (and without taking into account the better tax position thanks to splitting between two foundations).

Here’s the proof with an example of CHF 200'000 for the compulsory part:

- finpension 100% stocks at 6.58% annualized return: CHF 13'160

- VIAC 80% stocks at 6.11% annualized return: CHF 12'220

- Difference in favor of finpension: CHF 940

Therefore, finpension also wins the competition for best return.

5. Most favorable tax domicile (tax optimization)

finpension is located in the canton of Schwyz. And VIAC is based in Bâle.

If you withdraw your vested benefits to go abroad, the place where your vested benefits company has its registered office will be decisive for withholding tax on your pension capital.

Knowing that the lowest tax rate in Switzerland is in the canton of Schwyz with its 4.8%, finpension wins on this point (compared to 10.3% tax in the canton of Bâle for VIAC).

You could tell yourself that you’re staying with VIAC, and transferring your vested benefits to finpension just before you go abroad, but this will cost you money in special finpension fees (which they’ve set up precisely to avoid this type of behavior).

finpension is the best secured benefits option for 2026

After our detailed analysis according to objective criteria, I can therefore confirm that finpension is the best vested benefits option for 2026 for us Mustachians.

And to be clear: VIAC is still a very good option for earned benefits, the 2nd best in the whole of Switzerland to be precise, that’s quite something!

Details about finpension’s non-forfeitable benefits option

The more I look at finpension’s offering, the more I think they have a competitive advantage over VIAC: their independence.

Particularly for secured benefits, where finpension have, for example, been able to:

- Open two earned benefits foundations to enable splitting, and benefit from significant tax optimization

- React very quickly in October 2024, when the 85% global stocks limit was raised by the authorities (back to 100%), and inform all their clients straight away

It’s clear that VIAC is more dependent on WIR Bank on these points (even though WIR Bank is great, this adds a stakeholder into the mix).

Details about VIAC secured benefits

VIAC is still an excellent pension option. And they give their all for their clients.

When you stop working (and put your money into secured benefits), you mustn’t forget that your cover for incapacity and death also stop. VIAC has therefore decided to offer you — free — Life Basic cover of CHF 2'500 in the event of death or incapacity, for each tranche of 10 000 CHF that you invest.

And if you want to increase your cover, you can do this through their integrated Life Plus product (up to CHF 300'000 per death/incapacity) — with VIAC conditions (which are the bee’s knees).

Summary of the best vested benefits option for 2026 (in a table)

For the summary below, I’m using an example with CHF 200'000 for the compulsory part of the LPP:

| finpension | VIAC | |

|---|---|---|

| Maximum global stocks | ✅ | 🟠 (only the non-compulsory part) |

| Passive investing | ✅ | ✅ |

| Two foundations (splitting) | ✅ | ❌ |

| Return ranking | Tied 1st | Tied 1st |

| Favorable tax domicile | ✅ (Schwyz) | ❌ (Basel) |

| Fees | 2nd | 1st |

| Loyalty program | ✅ (CHF 25 of fees credit) | ✅ (free management of your first CHF 2'000 of pension fund retirement assets) |

| Fund providers | Swisscanto, UBS | Swisscanto, UBS |

| Platform languages | FR / DE / EN | FR / DE / IT / EN |

| Overall global ranking | 1st | 2nd |

The real-life example of the MP family

When Mrs MP and I become financially independent (meaning when we take very early retirement), we’ll put our LPP pension fund capital into two finpension vested benefits accounts, each held in a separate foundation.

Conclusion

In 2026, finpension is the best secured benefits option that is invested 100% in global stocks.

This retirement savings option enables you to store your LPP capital, and above all, to make it work to the maximum in order to increase your wealth.

VIAC is ranked second as they only offer the option to invest 100% in global stocks for the non-compulsory part of your vested benefits, which reduces your potential returns. Also, they don’t offer a second foundation for splitting in order to optimize your tax position.

It is important to note that vested benefits belong to the 2nd pillar (occupational pension) and are separate from the 3rd pillar (private retirement savings) and AHV/IV (state pension and disability pension).

===> MUSTBC <===

===> VBMust <===

FAQ 2nd pillar

What are finpension and VIAC’s other fees?

There are other fees applicable when you withdraw your vested benefits capital for buying a home for example, or use it as collateral.

You’ll find a recap of these fees in the table below:

| Fees | finpension | VIAC |

|---|---|---|

| Advance deposit (encouragement of home ownership / EPL) | CHF 500 | CHF 300 (and CHF 0 if you take out your mortage with WIR Bank) |

| Use as collateral (per case) | CHF 200 | CHF 0 |

| Transfer to another foundation (the same year as the contribution year) | CHF 400 | CHF 0 |

| Advisory and processing fees for withdrawing capital if domiciled abroad | CHF 500 (if with finpension > 1 year, otherwise CHF 3'000 + 1% of the vested benefits)) | CHF 0 |

Depending on your case, finpension’s vested benefits option may be less advantageous than VIAC (if, for example, you’re planning to withdraw all your capital from abroad during the first year after having placed your LPP with finpension).

What happens to my vested benefits account when I start a new job?

When you change employers, the legal framework stipulates that your vested benefits must be transferred to the pension fund of your new employer. In practice, however, the situation is more nuanced and allows for some flexibility. I explain this logic and its implications in detail here: What to do with your vested benefits account when you change employers.

What do you think of the VZ vested benefits account?

The maximum stock allocation for the VZ vested benefits account is 90%, which is less attractive than finpension.

Why don’t you mention frankly vested benefits?

Quite simply because this vested benefits provision from Zürcher Kantonalbank only offers a maximum of 75% in stocks.