My name’s Carole, I’m 45, married and I have 2 boys, aged 13 and 8.

I live in the canton of Fribourg, and I split my work life between a job at 65% (finance and administration manager) and self-employed work at around 20% (accounts, human resources and administrative matters).

So that’s me :)

I hesitated over writing to you for a long time but I feel that the world of financial independence lacks testimonies from women… so I went for it!

A happy childhood but a lack of financial education

I don’t think I’ve ever really been educated about financial matters.

I had a happy childhood during which I never wanted for any of the essentials, above all love.

But when it came to finances, I always saw my parents struggle! My father always spent money freely, and my mother had to do whatever she could to pay the bills… to this day, I still have great anxiety linked to my finances!

At the same time, I’ve always seen my mother work, and I’ve always said to myself that I would also be financially independent and would never depend on a man!

I’ve worked in order to be financially independent since the age of 14 by doing the grape harvest, then selling olives and mushrooms at markets, then in a pub and restaurant during my studies.

First salary, first financial mistakes

In 1999, I got my first job as an accounts assistant, and despite my careful relationship with money, well… I did what many young people do and blew it all!

And worse, I took out a credit card that I thought was like magic!!! After a few months, I realized that I had to get my finances under control; otherwise, I’d really land myself in it.

So there I was in 2001 with my first budget in Excel and realizing that my CHF 4000 salary would absolutely not allow me to live the high life. So I decided to be strict with myself, pay off my debts, and monitor my spending. It took a few months but I was able to start again with a clean slate.

But I still spent everything I earned… just not more!

Life with a partner

In 2002, I met the man who would become my husband and we decided to live together. I also decided to take an evening class in order to get a federal diploma in finance and accounting.

At that time, I was earning more than my boyfriend, and I wanted to travel, so I decided to combine all my money with his.

We managed to save for a holiday to Bali. We decided to get married and managed to save for the wedding, which took place in summer 2007. At that point, I still didn’t have an emergency fund, just a savings account at certain times for something specific.

The FIRE trigger: a Riad in Morocco!

But then… in 2008, we went to Morocco and fell in love with it!!! We started dreaming of having a property there and moving over there to live… except that we had zero savings!

I went back to my Excel spreadsheet, but this time with the goal of optimizing our savings.

Our first son was born in September 2009. The pull of Morocco was still there and the three of us made regular trips to the country. We also opened a savings account for our son into which we put CHF 100 per month.

In 2014 I fell pregnant with our second son. In June of the same year, we went to Morocco ready to sign the contract for our Riad that we were going to renovate. The asking price was €50'000, which we had. But at the moment of signing the contract, the vendor’s sons no longer wanted to. They asked for an additional €20'000, which we didn’t have.

So the sale fell through.

Our second son was born in November and gradually we forgot our Moroccan dream… It was difficult for us to travel regularly as a family of four. But we continued to save for this goal. In addition, we opened a savings account for our second son, into which we also put CHF 100 per month.

The second trigger on the road of becomming FIRE…

In 2016 my sister bought a property. It was a wake-up call! Why not us?!

We still had this dream of Morocco, but our eldest son had started school and maybe it would be better if our children went to school in Switzerland.

On December 23, 2016, we completed the purchase of our house! We were able to buy a property thanks to our savings and 2nd pillars. The house cost CHF 615'000 and required a 20% deposit. This was made up of 50% cash, 25% from my husband’s pension pot, and 25% from my pension pot (so CHF 32'500 from each 2nd pillar).

We thought that was cool, that good personal finance management was a great thing!

We thought that was cool, that good personal finance management was a great thing! But our accounts were completely empty! All our finances went on the house. We started from scratch again, and with even less, as despite the house purchase, we went on holiday with money that we no longer had…

Fall down and get back up again, always

So we racked up credit card debts (eek - bad idea!). After several months of living beyond our means, we said STOP! We went back to the Excel spreadsheet and once more resolved to budget, monitor our spending, pay off debts and save. And that was the point when I started to properly learn about personal finance (I also read your book on financial independance and FIRE).

I set up a savings account for our emergency fund, and I started to pay off all the credit cards.

In 2020, the company where my husband worked went bankrupt… His April and May wages weren’t paid and he didn’t receive the first unemployment payment until the end of June, with a 5-day penalty! I can therefore attest to the importance of having an emergency fund; it’s great! Although unemployment insurance meant we were able to get back the lost wages, we had to wait almost a year, so it was just as well that we had put some savings aside. Otherwise, we would have had to claim benefits or ask family for help!

By the end of 2021, we were finally free of all debt and even had some savings for our crazy plan to retire early to Morocco in 2034 (yes, yes, we were still dreaming of it, but in another form). We continued to save throughout 2022, and my husband went down to 90% during the summer, with every other Friday off! Nice for him! And then it came to 2023… we needed to invest, but, but, but…

Investing in the stock market… scary! Or not…

First block: my husband! He was scared. His view was that the money in the savings account is there, available and all ours. He suddenly decided that our emergency fund should be CHF 40'000 (NOOOOOO). In addition, he wasn’t keen on putting the maximum in a VIAC 3a pillar, as 3a pillars are locked, and if we needed the money for some kind of investment, and if and if… (small clarification: we each pay CHF 2820 per year into a 3a linked to our house, so we have a bit more leeway there).

And the second block: it was me and my fear… if I make a mistake with our family savings…

I was thinking about taking your stock market investment program, but first I needed to relook at the emergency fund. Or not? My husband said I could invest anything over CHF 40'000 (but not the children’s accounts), and never go below that. Personally, I’d like to have a lower emergency fund, like CHF 30'000 (that represents 3 months’ salary for both of us – we get around CHF 10'000 net per month between us). But is that too much?

In February 2023, I finally decided to purchase your stock market investment program, and agreed to the security savings amount of CHF 40'000 requested by my husband.

I studied the subject of investing in depth and learned loads of things, your program really is great for that!

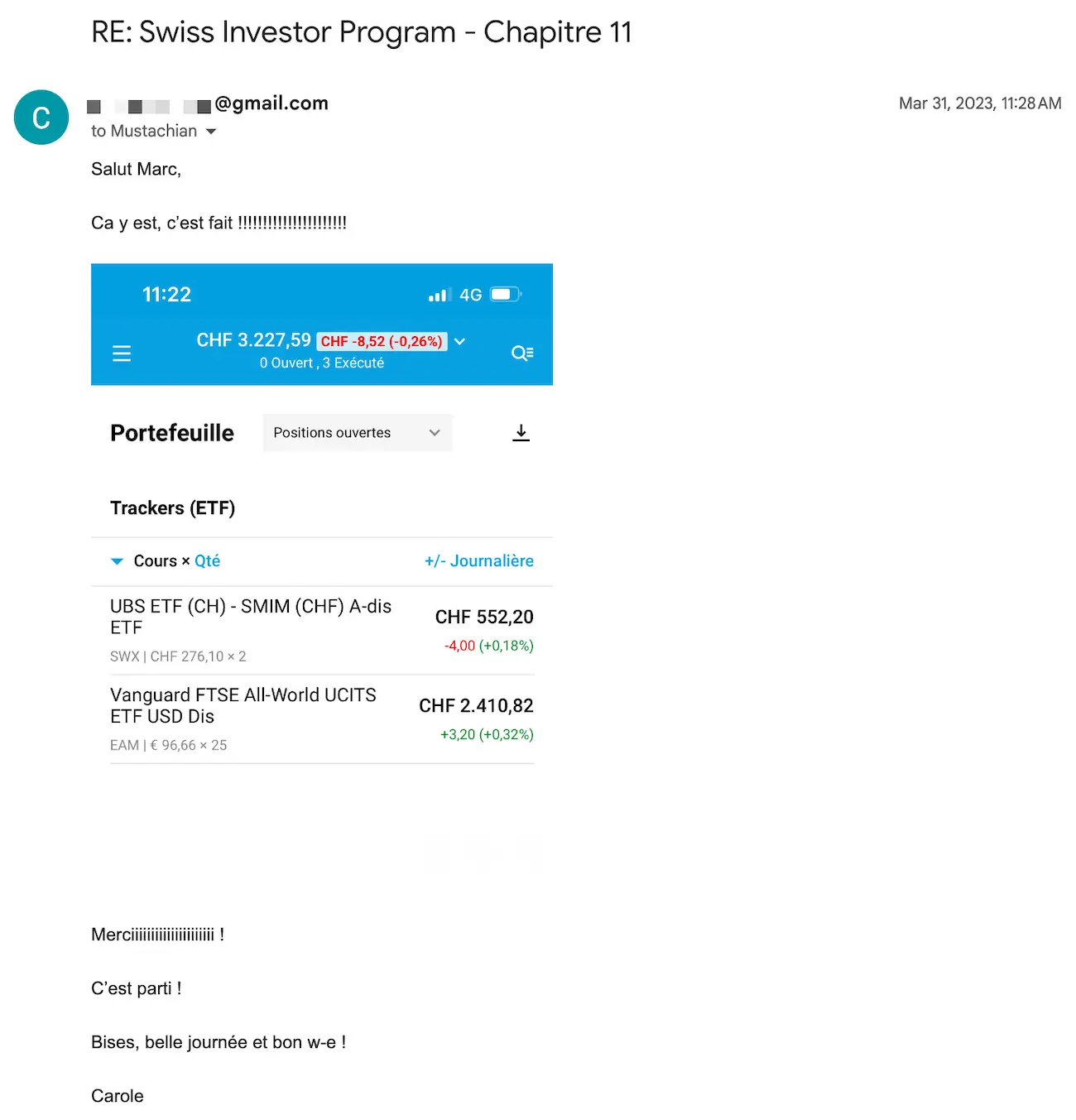

On March 31 2023, I took the plunge and bought our first ETFs. We decided to invest 25% in Swiss stocks and 75% in global stocks.

Since then, every month we have saved and invested via DEGIRO.

I must admit that when the Israeli-Palestinian conflict flared up again, the fall gave us a bit of a scare, but we stuck with it and we’re now very happy with it. The DEGIRO fluctuations have become a running joke between my husband and me!

Basically, the aim is to invest every month for our Morocco 2034 goal.

Relocation to Morocco in 2034

Moving abroad requires preparation, so I created a plan with several steps.

10 years can seem like a long time but it actually goes very quickly!

I’m fortunate (or not ^^) to be French-Swiss and so I can look into different scenarios of moving abroad. Tax address in Morocco or France? Create a real estate company in Morocco? Consideration of the advantages and disadvantages of each scenario, obviously with data that is valid today but not tomorrow.

But already, the first thing is to purchase the property quickly, in order to be able to use our working years to pay the real-estate off.

It’s now May 2024, when I’m writing this.

We are now faced with two large projects…

A language study year in London for the eldest son

The first is that our teenager wants to study English in London for a year at the end of his compulsory schooling in 2025.

I must say that we’re now pretty glad that we put CHF 100 into a savings account every month since he was born, then upped it to CHF 150 when he went to high school.

This has meant that we have no worries about being able to grant his wish and have begun to look into schools.

Our Riad purchase in Morocco

The second is our purchase of a Riad in Morocco.

So, we’ve decided to take the plunge.

We’ve been talking about buying real estate in Morocco since 2008, now we want to act!

We’re therefore looking to buy a small Riad (around 80 m2) in the Marrakech medina, renovate it and rent it out on Airbnb. It should be pointed out that Marrakech is developing rapidly and major milestones are coming up.

The Africa Cup of Nations in 2025, and above all, the World Cup in 2030!

Direct flights between Marrakech and New York have recently started up, and demand for accommodation continues to grow.

We have the funds to buy in cash (between 70'000 and 80'000 Swiss francs).

However, after a discussion with our neighbor, a real estate specialist for a bank, we’ve decided to try to take out an additional mortgage on our house, using the leverage effect. Our house was estimated at the beginning of 2023 and has gained in value (+ CHF 120'000 minimum) since we purchased it at the end of 2016.

And that’s THE good news from last week: the bank thinks we’re very thoughtful people. So they agreed to grant us an additional mortgage of CHF 80'000.

They would have gone as high as CHF 100'000, but we decided to be reasonable.

Now all we have to do is find the property of our dreams in Morocco — the search is on!

A look in the rearview mirror

If I look back at the path we’ve taken, I’m pretty proud of us, even though we could have done much better by being a bit thriftier!

I’ve calculated our net wealth at the end of 2021 and 2022, and it’s cool to see it grow like that, and to get closer to our goal of FIRE Morocco 2034!

For the more curious among you, here’s a quick update on the evolution of our net worth (made up of savings, LPP, our 3a pillars, our DEGIRO account, and the equity in the house):

- 01.01.2022 : 267'000.-

- 01.01.2023 : 296'000.-

- 01.01.2024 : 339'000.-

Thanks for your blog, Marc, and for your articles, which inspired me (especially from a Swiss person living in Switzerland), and also for your advice, not to mention your authenticity, which is so valuable these days!

MP comments

Carole’s story has prompted two thoughts.

Above all, I think she’s an example of perseverance. She took control of her finances every time. Try, fail, recover, retry, and move forward. As for many of us (me included), the path to financial independence is fraught with challenges linked to our human nature. But persistence is the key to success.

The second reflection is around the importance of having a concrete dream behind the desire to be financially independent. As the FIRE journey takes several years (10-15 years on average), it’s a dream that will keep you motivated — and not some financial goal in CHF.

We see this clearly in Carole’s example, especially with her fear of investing in the stock market. Without a life dream motivating her, I’m not sure that she would have dared to confront her fears and break through her glass ceiling.

And how about you, what is the dream that makes you follow the path to financial independence? (write to me in the comments or by responding to any of the email newsletters, I’d be interested to interview you like Carole)

Last updated: May 31, 2024