When I wrote my article on how to find the best mortgage, several of you mentioned the online solution Hypotheke.ch for comparing and taking out a mortgage online (with the best interest rates).

This prompted me to survey all the blog’s readers in order to find out if this was a recommendable solution.

Here are all the responses I received, as well as my conclusion at the end of the article — as well as a special Hypotheke.ch promo code for blog readers.

😃 Daniel D.

I’m of the opinion that the provider Hypotheke.ch is one of the best in Switzerland.

I always look at their homepage when I want to get an idea of the current offers. My subjective opinion is that this provider is one of the most independent in the sector. The majority of the other comparison sites are linked to a provider (insurance or bank).

I had a telephone call with one of the Hypotheke.ch team around 3 years ago (unfortunately I can’t remember his name, it might have been Mr Schubiger).

At the time, we were looking to remortgage with UBS.

We had an offer from UBS with a 0.6% margin for a Saron mortgage, so the Saron rate & then the bank margin of 0.6% on top.

I had briefly explained our financial situation over the telephone, the mortgage amount, etc. He immediately explained to me over the telephone that he believed that this was a very good offer and that I should accept the UBS offer. Which we did.

For me, this contact was very positive. We must have spent 20 minutes and more on the telephone, he listened to me quietly, asked me some questions and gave me his evaluation. It is highly likely that another provider would have immediately invited me to an appointment and then tried to “sell” me their service.

It is very likely that I’ll get back in contact with the provider if we want to remortgage in the future.

🙂 Jakub W.

I was looking for a mortgage in October/November 2024 and I decided to use MoneyPark and hypotheke.ch at the same time.

Overall, it was a good experience — communication was fast and professional, and they offered good rates from Migros Bank.

Unfortunately, I think they lacked a bit of flexibility and the capacity to manage more complex cases like mine — I already have a mortgage, and different banks interpret this in different ways (in terms of debt burden and income).

In the end, they weren’t able to get me a suitable offer and I went with MoneyPark and UBS.

😃 Lukas S.

I took out my mortgage with Hypotheke and I can confirm that it’s a very good service.

Here’s an overview of my experience:

- Conditions: SARON with a margin of 0,49%. It’s the best offer I could find on the internet, and they also offered me this rate without any issues.

- Online process: The process is based on an entirely automated work flow in which several pieces of information must be provided. This does require some effort, but is in line with what is required by other brokers.

- Support and completion: Once you’ve submitted most of the documents, they contact you and complete the formalities with you. The transfer from the old bank to the new one went smoothly without any issues.

In my case, everything went perfectly and I can definitely recommend them. I worked with MoneyPark for my in-laws’ mortgage a year earlier, which was also a very good experience. I’d say the two are as good as each other.

MP: “It’s interesting what you say about MoneyPark, as other readers have been a lot less positive since they were bought by Helvetia. MoneyPark or Hypotheke.ch, do you really view these two companies as comparable?”

The commercial model of Hypotheke.ch seems to be that they have agreements with companies who want to outsource searching for new customers. I ended up with Bank EKI, a cooperative bank which is very small, and which only has two branches. Hypotheke.ch appear to have an agreement with them to offer very good conditions in exchange for exclusivity over searching for customers for them.

Moneypark is different in this context. They have different partners, but seem to work on a non-exclusive basis. This was really good for my in-laws’ case, as the advisor looked for the best conditions based on their very specific situation. I think we were lucky with this, as the advisor we worked with was very customer-focused and probably sometimes even willing to make an additional effort above what was required of them from the company’s perspective. In short, I wouldn’t expect that to be the norm with Moneypark.

🤷♂️ SB

I’m sharing my notes with you from my contact with hypotheke.ch (Michael Bader), in May 2024:

- They are fairly active in German-speaking Switzerland.

- It’s not currently possible to get a mortgage offer for a rental investment building: but this should change in the coming weeks.

- At best they could perhaps obtain -0.1% on SARON and -0.2% fixed.

- By Mr Bader’s own admission, it’s not worth changing because the gain would only be around CHF 100 per month maximum for the debt of CHF 500'000.

- In addition, the change isn’t free: you need loads of documents, some of which require you to pay a fee to obtain them.

I should point out that my situation is somewhat unique with firstly a villa of 3 apartments in Montreux, which had to be remortgaged before my main residence in Fribourg. Hypotheke.ch wasn’t particularly interested in financing the rental property in Montreux…

I also looked into using VZ, but what annoyed me with them is that there were also intermediaries (internal) and they required powers of attorney to be signed. As I don’t really like giving up control, particularly at this level, I didn’t pursue this route.

As a public worker, BCBE’s offering for Publica policyholders is much more beneficial for me. Offer applicable to members of the APC – BCBE.

😃 Petra G.

Yes, I took out a mortgage with hypotheke.ch, and I’m very satisfied with them!

I read a review of hypotheke.ch in the Tages-Anzeiger.

I needed to remortgage in 2021. I registered with hypotheke.ch, I looked at their offers and I accepted one: mortgage from SGPK (St.Galler Pensionskasse) over 10 years at 0.65%.

I’d never have found it by myself, as I didn’t know that pension funds also provided mortgages.

😃 André G.

I remortgaged with this platform.

I have nothing negative to say.

Twice with no problems and fast.

It’s also possible to call Hypotheke advisors to clarify any questions.

😃 Manuela H.

Yes, I had a good experience with hypotheke.ch (but I ended up going with another provider).

Hypotheke.ch is without doubt a very good provider. Depending on your situation, you can get better offers elsewhere as hypotheke.ch is entirely automated (and therefore is less able to adapt to your specific needs).

From what I understood, one of their founders was previously at VZ Vermögenszentrum, and, together with an IT-savvy cofounder, they’ve built a web platform capable of automatically generating mortgage loan offers.

Their business model consists of offering users an easy-to-use platform for uploading all the necessary documents, and providing them with an immediate response confirming whether they meet the requirements of one of the providers in their network based on the information provided. Their involvement is minimal, but if you contact them by telephone (they’re really nice), they can help you and know exactly what you need to change in order to meet the minimum criteria of an offer. They also have some pension funds in their network which are not included/available with other brokers.

However, if you have specific/additional collateral (for example: an apartment already owned with another mortgage tranche), they have limited room for maneuver to make changes or reflect that in one way or another in their offer. I get the impression that a customer advisor in a bank or insurance company has more room to adapt the offer to your needs in this specific case. Overall, I liked the hypoteke.ch team and I recommend them to my friends.

What I’m not sure about: the time when you search for a financial partner and the point at which you fix the mortgage rate can be very different (in my case, the difference was 6 months), and it was obviously advantageous for me to wait as long as possible to fix due to the expected decisions by the BNS. I’m not sure that they (or their partner) are very flexible when it comes to adjusting/lowering the rate up to the day of fixing.

What is sure is that Hypotheke.ch is definitely better than the big competitors (Moneypark now belongs to Helvetia), as they try to understand your situation and help you as best they can to obtain the best offer they can get for you.

In summary: they are undeniably good with competitive rates, an efficient online procedure and a great team. It’s only if you have specific requirements for bespoke solutions that there can be competitors to take into consideration.

😃 John Galt

My bank (UBS) initially gave me a ridiculous rate despite me having been a good customer for 9 years!

I therefore used Hypotheke.ch and my friend has too over the past three months. I received very good support and offers which had no initial fees or obligations. Claudio was also able to negotiate the conditions after the first offer was approved, when my bank woke up and made a competitive offer in order to keep us — but the bank found by Hypotheke.ch made us an even better offer!

Verdict: I highly recommend Hypotheke.ch.

😃 Friedrich M.

I took out a mortgage through their intermediary at the end of last year, and I must say that I’m very satisfied with their service.

The central service worked very well.

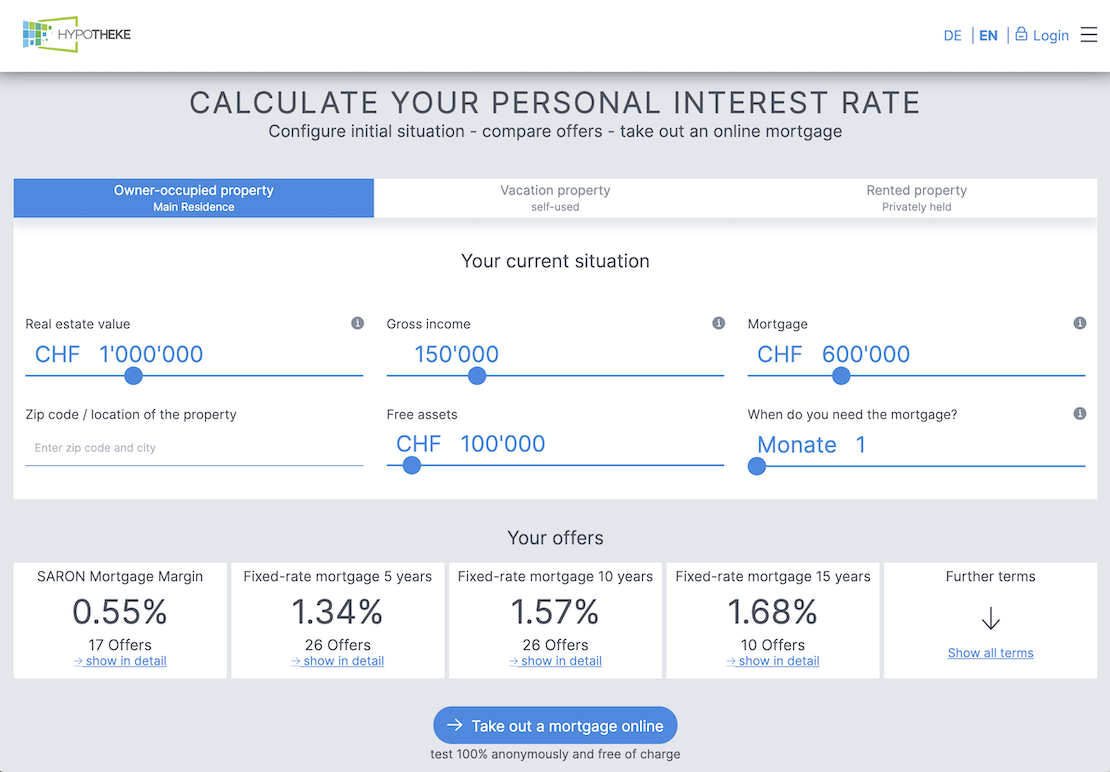

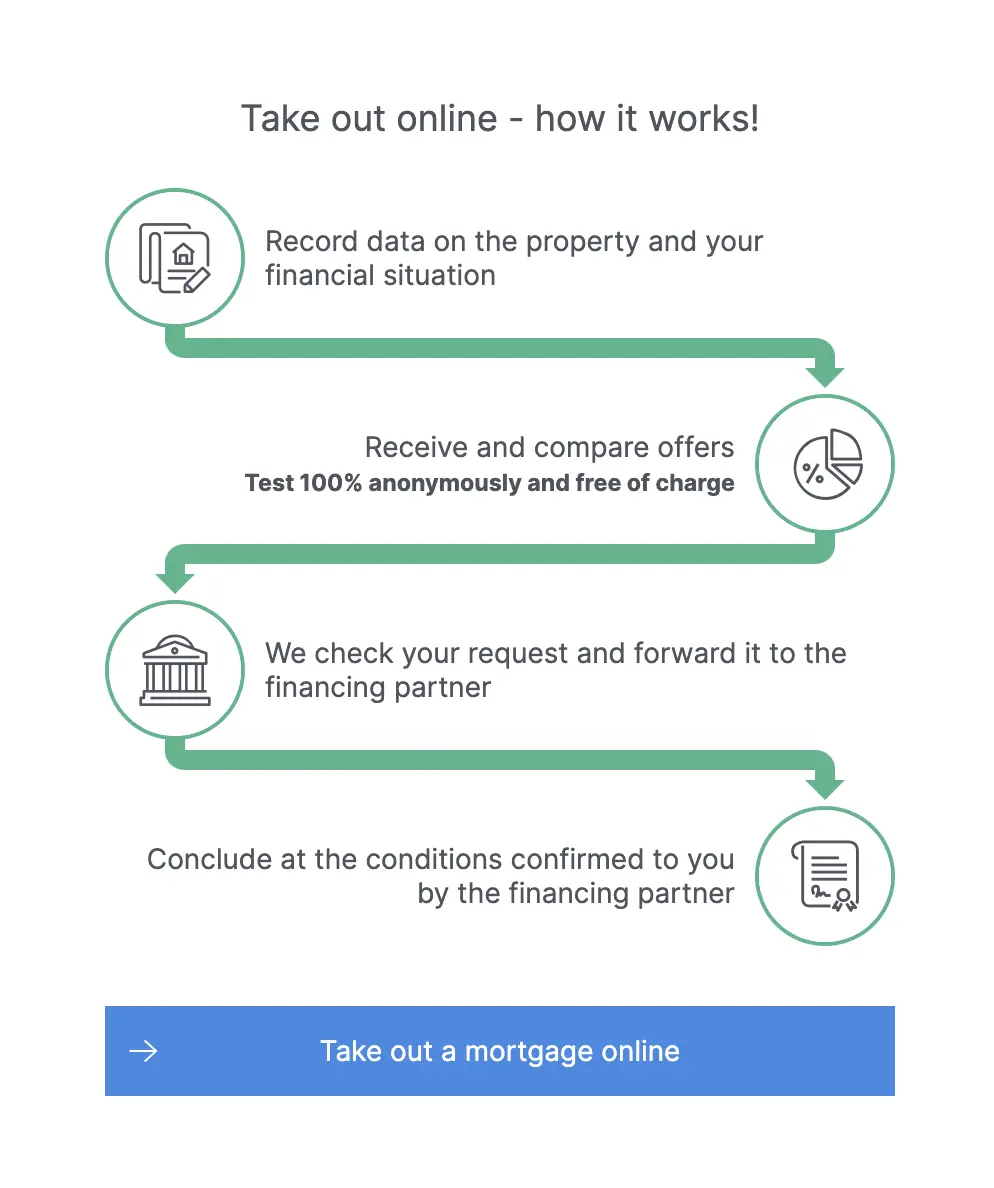

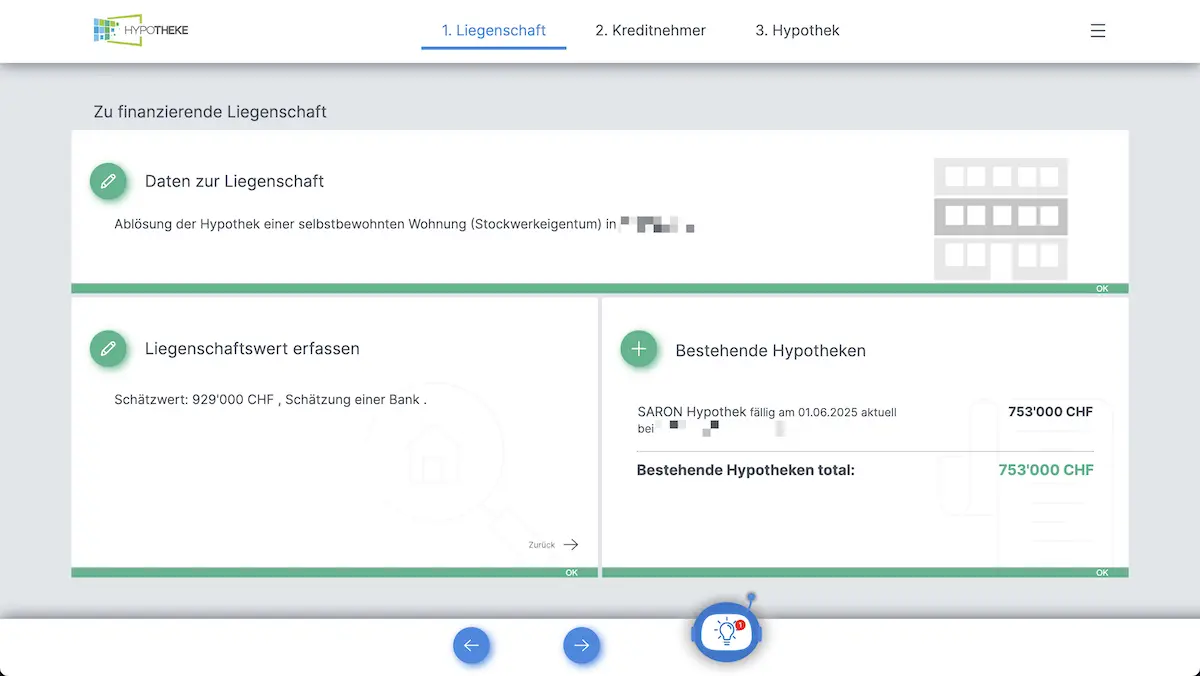

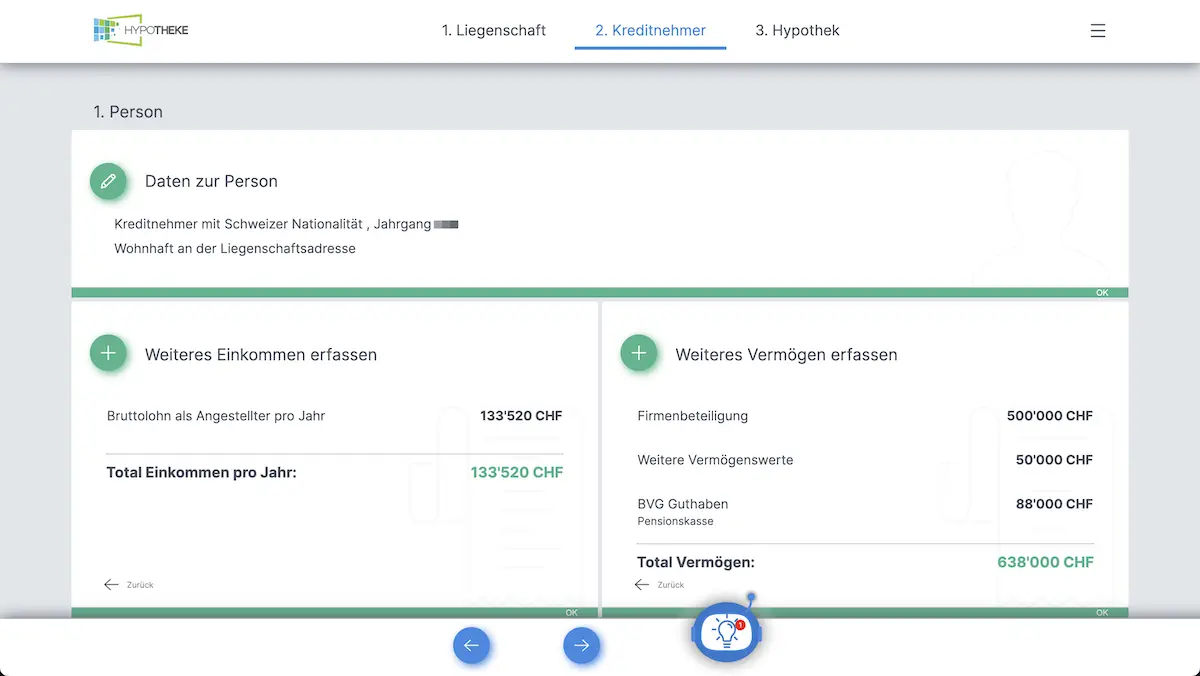

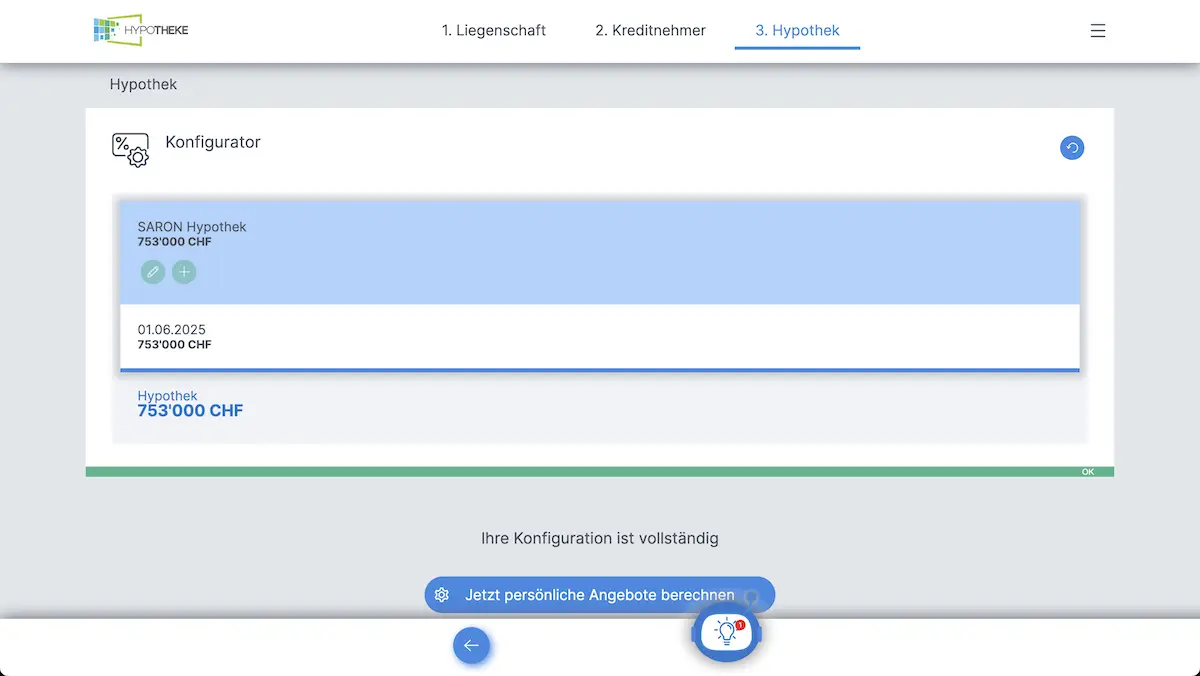

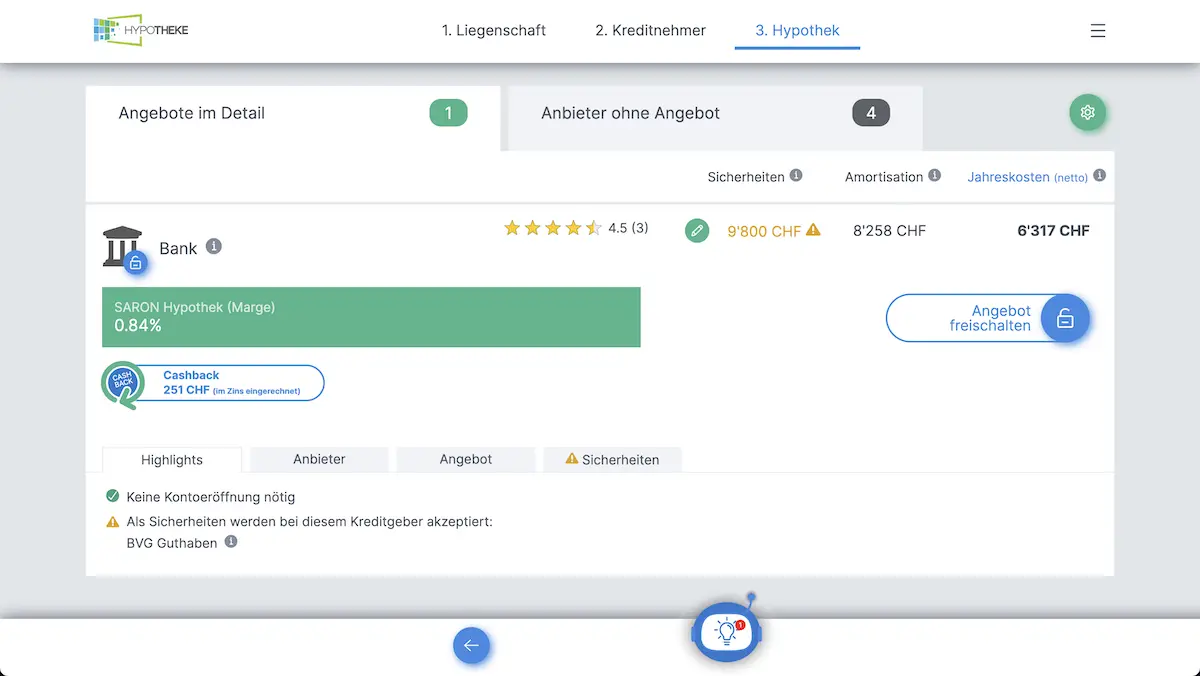

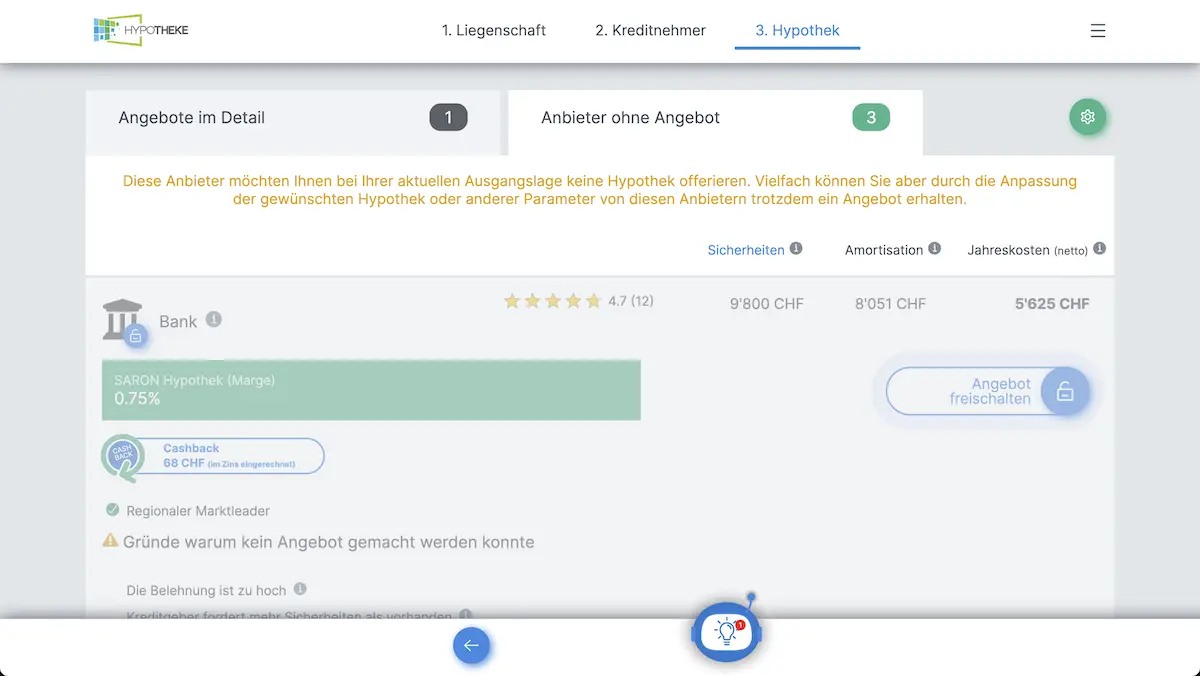

How the Hypotheke.ch service works

It’s very quick and easy to get real mortgage proposals:

In this other tab, I've got mortgage proposals that will come through if I change certain parameters (I can also call Hypotheke.ch to ask them for help in real time)

The user experience is very straightforward and efficient. I’d prefer a design that’s a bit more modern but, in the end, for taking out a mortgage or remortgaging once every X years, that’s a minor detail.

MP conclusion regarding using Hypotheke.ch for your mortgage in Switzerland

Frankly, I’m amazed to have received so many positive, even very positive, opinions.

Let’s be honest: as a Mustachian, we’re demanding and meticulous when it comes to anything related to personal finance.

I hope that the Hypotheke.ch team will be able to manage its growth, while maintaining this level of customer service. But in fact, I believe that this mindset comes from the cofounders, who have a long-term vision (rather than short-term in wanting to sign contracts at any cost). I like that!

I also really liked it when Lars Schultz (their CTO and one of the three cofounders) told me when we were chatting about the English version of their site:

I personally like our service, as we can talk freely about (almost) everything with our customers, as we work hard to ensure that everyone (the customer, the mortgage broker, and us) gets treated fairly.

If I had to remortgage today, I’d request a proposal for a SARON mortgage from:

Then, I’d make a comparison table with all the criteria mentioned in this article (it’s not just the rate that counts!), and I’d choose the best mortgage.

Promo code Hypotheke.ch

You can specify the code "MPHYPO" to the Hypotheke operator when you take out your mortgage. This will entitle you to an additional cashback of CHF 100. And the blog will also earn a small commission in the process, for which I thank you.

FAQ Hypotheke.ch

Is it possible to use a 100% stocks 3a pillar for indirect amortization?

The majority of non-bank lenders accept this type of collateral, i.e. pension funds, investment foundations and insurance companies.

However, they won’t take 100% of the value of this type of 3a pillar into consideration, due to the risk inherent in stocks portfolios. Therefore, if you have CHF 100'000 in your VIAC or finpension account, some lenders will only count it as 60 or 80'000 CHF for collateral.

How does Hypotheke.ch make money? What do I have to pay as a customer?

For a standard case, Hypotheke.ch customers don’t generally have to pay anything, as the broker’s commission usually covers all their expenses and fees.

In almost all the cases they’ve had up to now, the customer even receives cashback on top (in cash, paid directly into your bank account). This cashback is communicated transparently in their tool, even before the customer provides their email address.

The way they work is very simple: they calculate the fees for each case, based on the mortgage amount and the duration of the contract, in the same way as most mortgage brokers calculate their commission, except that their fees are a bit lower.

As their fees are always calculated in the same way, where the mortgage is taken out is irrelevant to them.

Then, the customer receives the difference between the commission and Hypotheke.ch’s fees in the form of cashback. If this ends up being nothing or if the fees are higher than the commission, the customer will have to pay the remaining fees, but they are usually practically zero.

The cashback or the remaining fees are always clearly indicated before the customer chooses an offer.

The only situation in which they request (partial) fees is if the customer withdraws after a clearly communicated stage, which is quite late in the process.

Why would banks and other institutions want to work with Hypotheke.ch?

The mortgage lenders on the platform also benefit from their unique process because, in general, they only submit an application to the one lender chosen by the customer.

This is contrary to the traditional process, which consists of submitting an application to several lenders with the intention of obtaining an offer from each of them, which only one of them will end up having accepted.

The application is checked and complete, ready to be signed off by the lender, as the Hypotheke.ch teams have already checked that the application fulfils the lender’s criteria.

They told me they have a very high conversion rate for applications submitted to their lenders, as they check the information given by their customers against the official documents provided in support.

Is Hypotheke.ch available in French?

Unfortunately, they don’t currently have the necessary resources to be able to offer their services in French.

It’s obviously on their to-do list, but up to now, they haven’t had the time to do it and as they’re a small company, they really need to concentrate on their core work.

But they are aiming to provide multilingual support during the coming year (2025). English should be fine on the telephone with their advisors, but their online content has not yet been fully translated.

Do I have access to all the offers without having to pay?

Their mortgage rates are calculated instantly for more than 30 mortgage brokers, so the customer is always able to choose the best offer, and everything, except the name of the mortgage broker, is available for the customer while remaining anonymous.

In order to communicate the names of the mortgage brokers linked to the offers, they request the customer to identify themselves by providing and confirming a mobile telephone number.

How long has the Hypotheke.ch service existed?

They started developing their app in 2016, and founded the company in January 2019.